Crossing Borders

The Revival of European Bank M&A

Twenty years ago, give or take a few months, I was finishing up a meeting with the chairman of HVB Group, one of Germany’s largest banks, at his offices in Munich.

“You know, UniCredit in Italy may be interested to acquire us,” he said as I was putting away my notebook.

Doubtful, I thought. HVB Group had been formed six years earlier in a hurriedly negotiated merger between Bayerische Hypotheken- und Wechselbank (Hypobank) and its cross-town rival Bayerische Vereinsbank, whose management was eager to stave off a hostile bid from Deutsche Bank. Within months of the deal closing, a €1.8 billion hole in Hypobank’s property lending book was uncovered. Executives from either side fell out and the group struggled to integrate. “He is consumed by vanity and unfit to run a bank,” said the former boss of Hypobank, from his perch on the supervisory board, about Albrecht Schmidt, head of the combined group.

My meeting was with Schmidt’s successor, Dieter Rampl. Rampl had inherited the second largest bank in Germany, the tenth largest in the world by assets. With 4 million customers, it had 5% of the retail banking market in the country and 15% of the market in the wealthy region of Bavaria. But its credit portfolio remained a drag, particularly in real estate where commercial property prices continued to slide. “Our greatest weakness is the size of our loan book,” Rampl wrote in his 2002 annual report.

Rampl launched a number of initiatives to shore up his bank’s balance sheet. He spun off a portfolio of property loans into a new company to reduce real estate exposure; he sold trophy assets including a stake in Bank Austria, which the group had acquired in 2000, to raise cash; he suspended dividends; he completed a €3 billion capital increase. As quickly as he moved, though, new problems arose and thin margins in the group’s core business – an issue we discussed in The German Bank Paradox – deprived him of cover. Rampl’s goal to generate a return on equity in excess of 10% looked increasingly out of reach. In 2003, the bank incurred a net loss of €2.6 billion and, in January 2005, it warned that 2004 would be no better after it was forced to write off a further €2.5 billion of property loans.

Downing a half-liter of Paulaner at the airport, I wondered why UniCredit would want to get involved.1

A few months later, the deal happened. It was a Sunday in June and I received an invite to an impromptu analyst meeting in the City of London that evening. Rampl was there alongside Alessandro Profumo, CEO of UniCredit. The pair trumpeted the strategic rationale of the deal. It would create “a strong new force rooted at the heart of Europe with three neighbouring home markets straddling one of the continent's most prosperous regions,” said Profumo, talking about Bavaria, Austria and Northern Italy. “With this transaction, UniCredit and HVB are at the forefront of the European banking consolidation, which has enabled both of us to choose the best partner,” added Rampl.

Pan-European banking integration was on. Previously, consolidation had taken place within markets but little had spilled out across borders. Yet a single currency made the prospect viable and although modest branch overlap limited expense savings, central functions could be combined to reduce costs. UniCredit and HVB projected €985 million of annual synergies by 2008 (on a combined cost base of €12.9 billion), 90% to come from lower costs and 10% from higher revenues through “sharing of best practices”.

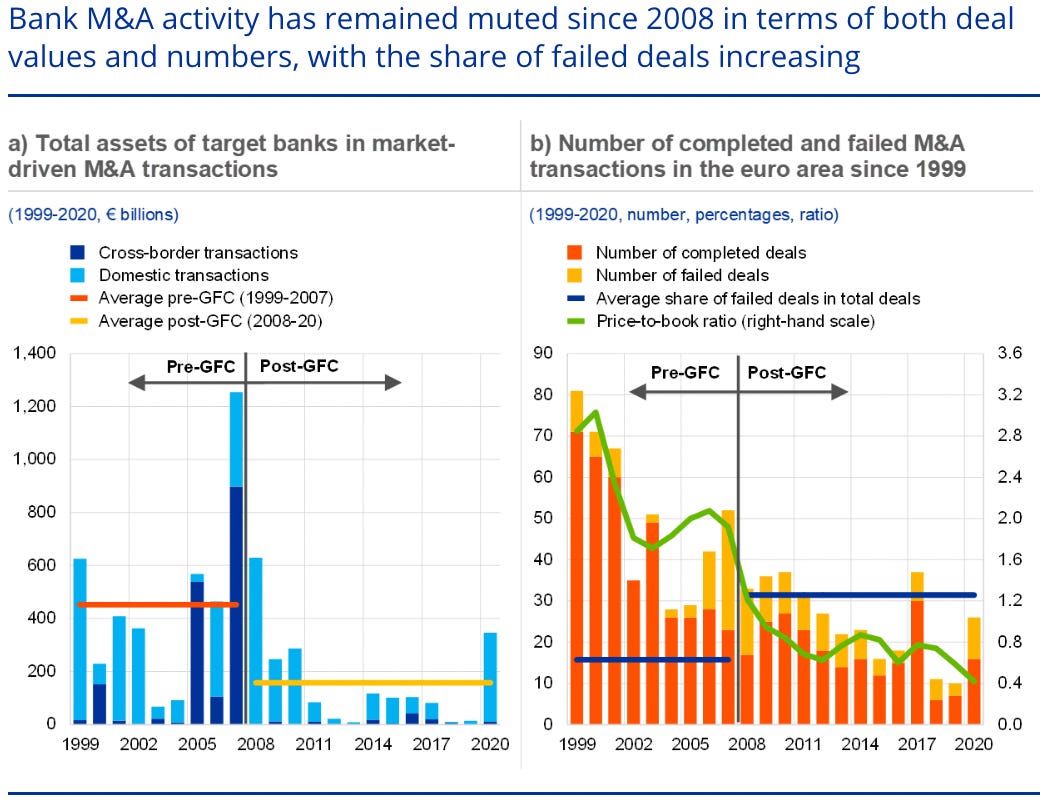

By the time 2008 rolled around, it was difficult to validate how much value the deal had created: A financial crisis was in full flow and UniCredit had gone on to do other deals including the acquisition of domestic rival Capitalia to make it Europe’s second largest bank, the sixth largest in the world. Although UniCredit survived the crisis, cross-border tie-ups that followed its lead didn’t do so well and urgency to do deals evaporated. Since the financial crisis, euro area banking M&A activity has fallen by around two-thirds and within that, cross-border accounts for less than 20%.

But this week, UniCredit signaled that it might be back in the game. When it bought HVB, the bank was advised by Merrill Lynch banker Andrea Orcel. Orcel is now CEO of UniCredit which this week took a 9% stake in German bank Commerzbank. “The ultimate goal is what everyone talks about: Europe needs stronger banks. Europe needs cross-border,” he told Bloomberg TV.

So is this the start of a second wave of cross-border banking M&A in Europe? Will remaining candidates feel an urgency to pair up before the best partners are taken? Will UniCredit even go through with a full takeover of Commerzbank? To dig further, read on.