The Five Families

Inside the Brokerage Industry

“How much did we lose today?”

“A billion.”

“And yesterday?”

“A billion.”

Short-selling is not easy, as Gabe Plotkin, ex-hedge fund manager, knows. Caught on the wrong side of a massive short squeeze, his fund, Melvin Capital, lost 54.5% of its value in January 2021, or roughly $6.8 billion. Although Plotkin did recoup some of his losses, he ended up closing his fund sixteen months later. His story makes it to the big screen next week with the release of Dumb Money, a movie about the GameStop trade at the heart of his losses and the meme stock frenzy it inspired.

Every finance movie has a neat way to explain a financial concept, and it’ll be entertaining to see how Dumb Money does short selling. In the film Rogue Trader, Ewan McGregor explains how financial futures work with reference to a cappuccino. In The Big Short, Ryan Gosling uses a pile of Jenga blocks to demonstrate how a mortgage-backed security can unravel. The book on which Dumb Money is based uses donuts to explain short-selling:

“Let’s say that donut is GameStop stock,” says amateur investor Kim Campbell. “And let’s say the current market price for that donut is five dollars. And I’m Melvin Capital. I think that donut is garbage. So I borrow it from you.”

“We make an agreement that I have to give the donut back to you in a couple of days,” she continues. “So I sell the donut into the market, for five dollars, the current price. And I wait. Planning to buy it back and return it to you when the price goes down, pocketing the difference.”

I don’t know whether they’ll roll with the donut analogy in the movie – I’ve only seen the trailer – but it hits the key point: In order to sell short a stock, you first need to borrow it – you can’t (legally) sell what you don’t have.1

The plumbing behind the borrowing process is unlikely to have made the final cut of the movie, but it’s an interesting subplot that’s worth exploring.

To get hold of the stock, Gabe Plotkin would have had to call one his prime brokers. (Plotkin is played by Seth Rogan; I’m not sure who central casting lines up as the prime broker.) He had four: Goldman Sachs, JPMorgan, Morgan Stanley and National Financial Services (a subsidiary of money management firm Fidelity). The prime broker’s job is to locate the stock from among its owners and facilitate its loan to Melvin in return for a fee that would be shared between the broker and the lender. For the stock’s owner, the lending fee provides an ancillary stream of income that can help to boost returns.2

Stocks with low levels of “short interest” are normally easy to borrow. For most large non-financial stocks, short interest tends to be less than 2.5% of the shares outstanding; for smaller stocks, it can rise to around 13%. In GameStop’s case, short interest was persistently much higher.

As long ago as 2012, short interest in GameStop amounted to half the total volume of shares outstanding. That level was hit again in 2015, 2016 and 2018, before rising even further in 2019. For the short-sellers, the trade seemed like a no-brainer. “GameStop had an archaic business model,” the book notes, “selling new and used video games in physical stores, while the market was being overtaken by digital downloads via the Internet.”

Between 2019 and early 2021, GameStop short interest hovered around 100% – every single share in circulation was also sold short. In rare cases, short interest can exceed 100% if the person buying the stock from the short seller immediately turns around and lends it out again, and in December 2020 GameStop short interest hit a high of 109%. By then, people were really keen on shorting GameStop.

“Wall Street is betting that this company is going to fail,” chimes in Kim Campbell’s character in the movie. “And if it fails, these hedge fund assholes make a shit ton of money.”

But GameStop didn’t fail. Indeed, just this week, it beat revenue expectations. Not that its stock was tethered to fundamentals much. The meme stock phenomenon drove its price up 1,700% from around $5 at the end of 2000 to $87 at the peak and shorts like Plotkin lost a lot of money. For a while, stockholders made money before the stock drifted back (it currently trades at $18).

Along the way, stockholders also picked up fees from stock lending. Typically, stock lending fees average around 1.5% but during the second quarter of 2020, the lending fee on GameStop went as high as 100%, driven by the heavy demand for borrow. Although it declined to under 50% by June 2020 and 25% in January 2021, by normal standards it remained very high throughout.3

While there were winners and losers on both sides of the trade, those in the middle – the brokers – were only winners. We’ve dug into the business model of retail brokers here before, companies like Robinhood which facilitate trading for individual investors such as Kim Campbell. Robinhood generated record earnings over the period GameStop went 🚀🚀🚀.

The challenge with that model is that margins have been competed away. Retail brokerage commissions collapsed from $40-60 per trade in the mid-1990s down to zero today, with “payment for order flow” replacing commissions as the dominant, albeit controversial, revenue model – all themes we’ve discussed before.

The market for stock lending, though – the one Goldman Sachs, JPMorgan and Morgan Stanley play in – remains a lot more attractive. Several features make it so:

Stock lending is an “over-the-counter” (OTC) market which means there is no central marketplace or exchange that allows participants to send their bids and offers to the entire market or obtain real-time trading data such as price and volume information. Instead, intermediaries serve as gatekeepers, enhancing the profits they can extract. By keeping data about prices and volumes hidden from the market as a whole, they are able to benefit from higher margins that flow from opacity.

It’s also a very big market. According to the International Securities Lending Association, $2.6 trillion of securities were out on loan at the end of June 2023, split roughly equally between government bonds and global equities. In the last 12 months, owners of these securities earned $13.4 billion of incremental income in lending fees. Although GameStop is no longer as big a short as it was, cinema chain AMC – another early meme stock – is. (An AMC theatre would be a very meta place to watch Dumb Money.) In the first six months of the year, AMC shareholders captured over $450 million of fees through stock lending. Overall stock lending revenues are up 27% since the first half of 2021 – a period where retail trading revenues are down.

Finally, it’s a highly consolidated market – all the more so since the exit of a number of prime brokers in the wake of the Archegos fiasco. Based on the number of hedge fund relationships they have, the top five prime brokers have a 58% share of the market and the top three – Goldman Sachs, Morgan Stanley and JPMorgan – 44%.

These dynamics make stock lending a very profitable business. Brokers capture a cut of the lending fees, typically between 5% and 20% of total earned income, and these add up. Back in 2015, Goldman Sachs revealed in court filings that it had made an average $830 million a year in revenue from US securities lending in the two years prior to the 2008 financial crisis. Those revenues contributed 75% of the overall revenues it generated in prime brokerage in the Americas, and 51% of the revenues it generated in prime brokerage globally.

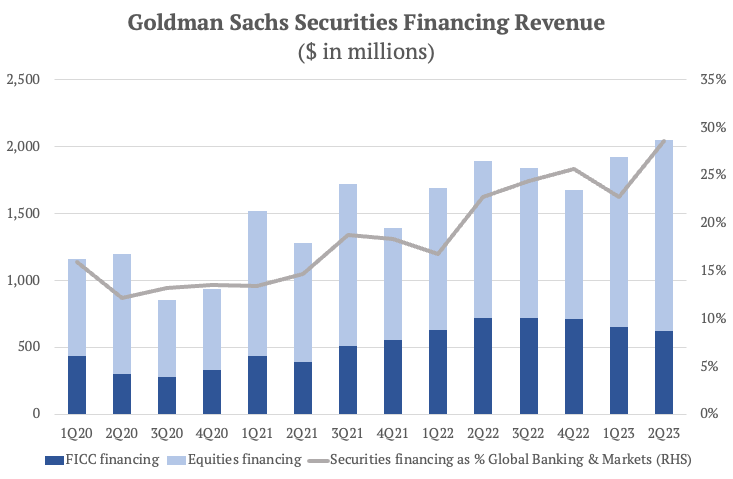

Since then, it hasn’t published details of its securities lending revenues, but overall securities financing income – of which securities lending forms a part – has grown to make up a quarter of the group’s investment banking segmental revenue. In its latest quarter, the bank spotlighted the record revenues it generated in its equities financing business.

You’d think a market like this would have invited more disruption, right?

Wrong.