When the Ducks are Quacking

SpaceX, Anthropic, OpenAI and the Business of IPOs

“We are definitely in a moment where there is more greed than there is fear… Base advice over 42 years of doing this: When capital is available – if you’re capital consumptive and it’s available – take the capital if you know that you’re going to need it.” — David Solomon, Chairman and CEO, Goldman Sachs, June 2026.

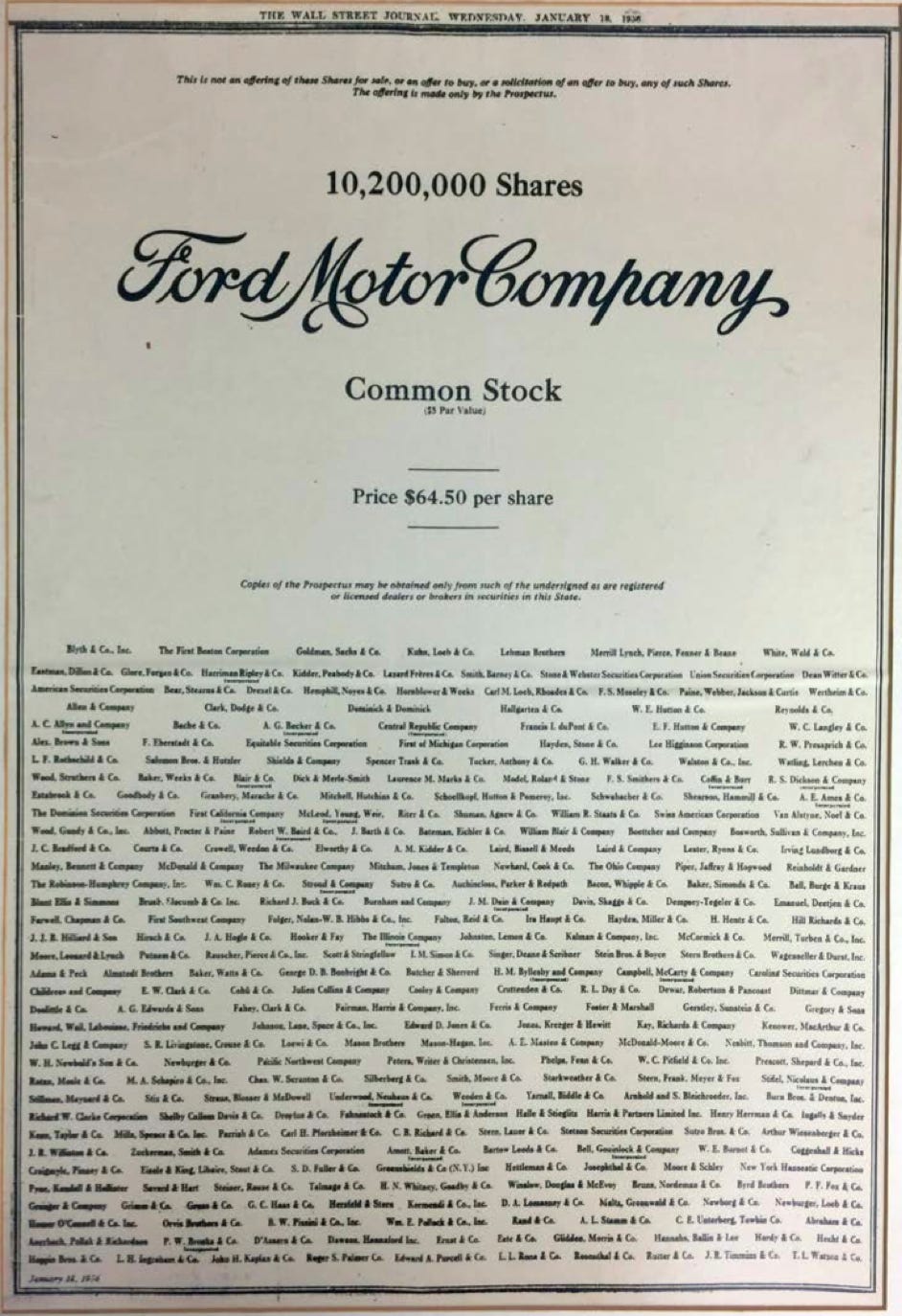

Today it would rank only tenth, but when it came to the market in January 1956, Ford’s was the largest initial public offering in US history.

It was a long time coming. The company had been founded over fifty years before and had remained private throughout. Early investors had long since cashed out so there was no clamor for liquidity. Indeed, their success was legend. Everyone knew the story of James Couzens – later Senator Couzens – who scraped together $2,500 to invest in the new Ford Motor Company in 1903; in 1919, Henry Ford bought him out for $30 million. So when the public were finally invited in, the response was unlike anything Wall Street had seen.

The selling shareholder was the Ford Foundation. To mitigate estate taxes, Henry and his son, Edsel, had transferred almost 90% of the company’s stock into a foundation in 1936. Although technically a philanthropic endeavor, the Fords used it to safeguard family control. Henry died in 1947, Edsel before him in 1943, and by the mid-1950s the Foundation was keen to diversify. Its endowment was substantial – by this time, Ford was one of the largest private companies in America – but its income consisted entirely of Ford dividends, too unpredictable to plan around. Selling shares was the solution.

Yet before an IPO could take place, the Foundation needed to overcome a problem. Its economic interest in Ford didn’t extend to voting rights, which remained firmly in the grip of the family. Foundation president Horace Rowan Gaither didn’t think shares were marketable without them – and the New York Stock Exchange agreed. The family and the Foundation turned to Wall Street for help.

A solution took two years to negotiate but Goldman Sachs senior partner Sidney Weinberg, working with assistant John Whitehead, eventually got there. Operating in total secrecy – Ford was never referred to by name; in all correspondence it was simply “X” – they presented over fifty different proposals. In the end, the family gave up their exclusive voting rights, transferring 60% to a new class of common stock in return for an increased equity stake worth around $60 million.

Goldman leveraged this advisory work into a major role in the IPO syndicate. It wasn’t technically lead bookrunner – that role fell to Blyth & Co – but Weinberg retained significant influence over the process. For their part, Blyth & Co were surprised to win the mandate, the firm’s own head of syndicate admitting he had no idea how they’d done it. “What I do know,” he told journalist John Brooks, “is that one day in November, Mr. Gaither called Mr. Blyth, our chairman, who was in San Francisco, and asked him to fly to New York right away. When the head of an organization that’s about to sell something like half a billion dollars’ worth of stock asks an investment banker to come, he comes.”

Including Blyth and Goldman, seven lead underwriters were appointed as part of a syndicate that stretched to 722 firms. The only names not on the list were Morgan Stanley for its ties to General Motors and Dillon Read for its ties to Chrysler. “The syndicate will include just about everybody who’s in the business and who isn’t, or hasn’t been, in jail,” a Blyth vice-president told Brooks.

These days, it would be difficult to identify 700 firms and indeed many have disappeared – including Blyth, which was absorbed first into PaineWebber and then into UBS. John Whitehead, who later became Goldman chairman, kept a framed copy of the tombstone advertisement listing these firms in his office and would cross off names with a red pen as they failed, merged, or changed name. By the end of his tenure, few were left.

On January 17, 1956, representatives from each of the underwriters (bar one, banned from trading in New York over a shady Alaskan securities promotion) filed through Blyth’s offices to sign their underwriting agreements. On behalf of them all, Blyth agreed to pay the Ford Foundation $63 a share for 10.2 million shares, to be distributed to clients at a $1.50 mark-up.

By then, prospectuses had been mailed (half a million copies of a preliminary prospectus plus more than a million of the final prospectus), ads placed (in 120 newspapers), a due diligence meeting convened (where people scrambled to catch a glimpse of Henry Ford II) and demand gauged. It was to be “a landmark in the history of public ownership,” declared the president of the New York Stock Exchange, “as hot as a firecracker,” Blyth’s head of syndicate told Brooks.

Unsurprisingly, the deal was oversubscribed. Around 5-10% was reserved for institutional investors, 10% for Ford dealers and employees, and the rest would go to the public. Normally so disdainful of IPOs, even Warren Buffett bought in. “I haven’t bought an initial public offering since 1955,” he said a few years back. “I bought 100 shares of Ford when it came out. Gus Levy [Goldman’s head of trading] was running it. As a favor, he gave me 100 shares and I have to admit it now – I think the statute of limitations has expired – I took a free ride on 100 shares and made $500 and it’s the only time I’ve ever done that.” (He was making $12,000 a year at the time, he said, and $500 looked very good.)

Ford stock opened for trading on January 18 (ticker: F) with around 300,000 new owners. It traded up to $70.5 that day, handing them an immediate gain of 9.3%. But over the next few months the price drifted down into the forties as Ford dealers, who had overextended themselves to buy stock, rushed to sell.

By then, the banks had made their money. Their $1.50 per share mark-up rewarded them with fees of $15.3 million, equivalent to 2.33% of the funds raised. After expenses, they were left with 2.17%. As a high profile deal this fee rate fell on the low side. A few years later, Blyth brought publishing house Grosset & Dunlap to market for a 5.5% fee. Smaller deals attracted fees as high as 15% and often included warrants and expenses charged to the issuer that could push rates above 25%.

Goldman earned an additional fee of $250,000 for its advisory work and while this, too, was low – the work was thought to be worth $1 million – it set the firm up for a long business relationship with Ford. Weinberg hung a note he received from Henry Ford II on his office wall: “Without you, it could not have been accomplished.” He joined the Ford board and for nearly half a century Ford would become Goldman’s most prestigious investment banking client.

When Goldman itself IPO’d in 1999, Ford played a part. William Clay Ford Jr., then the carmaker’s CEO, was given an allocation of 400,000 shares – the largest allocation to an individual. A Ford shareholder sued, alleging the allocation was a reward for Ford’s business with Goldman Sachs and claiming that any gain on the shares belonged to the company. Ford agreed to settle, receiving $10 million from Goldman Sachs, and Bill sold his shares, donating the $4.5 million profit to charity.

Goldman has done a lot of IPOs over the years. It is leading the upcoming SpaceX IPO and has just been picked to lead on Anthropic. The record-breaking $85 billion secondary offering it organized for Google this week adds to its capital markets pedigree. Some things have changed since Ford – others have not. To see how the IPO business has evolved, and what the SpaceX IPO heralds, read on.