TPG: A Tale in Five Trades

Plus: CUSIP, Western Union, Banker Bonuses

This is a free version of Net Interest, my newsletter on financial sector themes. For additional content and supplementary features, please consider becoming a paying subscriber.

Investment managers operate strategies across many different timescales. Hedge funds think in terms of quarters and years, high frequency traders in minutes, private equity firms in decades. While a hedge fund may do hundreds of trades over a year, it would take a private equity fund decades to do so many trades.

We’ve talked about private equity a fair bit here before. A year ago, in The Private Equity Firms' Private Equity Firm, we looked at how the industry is structured and how it makes money. More recently, we drilled down into the business model of the biggest player in the market, in Blackstone's Moment.

Ahead of its upcoming stock market debut, this week we turn our attention to TPG.

TPG is coming up to thirty years old but over that time it’s done just over 640 trades. Granted, these are big trades – whole chunks of companies, from A&O Hostels to ZScaler. And trading frequency has increased – three years ago, the firm had only ever done around 460 trades. But 640 is a manageable number of trades to look at. If you wanted to, you could review every one of them to get a handle on TPG’s process – a useful exercise for any prospective investor in either the firm’s funds or its stock.

We’re not going to do that today, but it could be instructive to look at a few. So let’s take five. We’ll look at TPG’s first ever deal and one of its most successful (Continental Air), its worst (Washington Mutual), one of its most messy (Caesars), one it double-dipped on (J Crew) and one that distinguishes it from traditional private equity firms (Uber). Along the way, we’ll see how TPG conducts its investment business in an effort to see what’s in store for investors.

1. Continental

The 1980s was a rich time for corporate activism and one man, his fortune originating in Texas oil, was heavily involved. Robert Bass had already made a number of big-ticket investments in partnership with his brothers – they once held a 16% stake in Disney – but in 1985, he set up a personal investment vehicle to go it alone. He hired a team to help, including two men: a lawyer a few years his senior, David Bonderman, and a Stanford MBA, James Coulter. Over the next few years, Bass and his team went beyond stock investing to finance entire corporate buyouts, striking deals across media, manufacturing, hotels and banking.

In 1993, Continental Airlines appeared on the Bass team’s radar. The company was coming out of bankruptcy and Bonderman thought it was worth a look. Bass wasn’t convinced. As well as being in a weak financial condition, the company faced protracted labour disputes and was still reeling from the recession of the early 90s. But Bonderman was certain the deal had potential and so, with Bass’s blessing, he and Coulter formed their own investment vehicle to pursue the opportunity. They raised $64 million (including some from Bass) and, in partnership with Air Canada, they took it on.

Immediately after closing, Bonderman became chairman of Continental and installed a new CEO. Together, they embarked on a full scale turnaround, targeting all areas of the company from baggage handling to food to customer service. It didn’t take them long to improve Continental’s fortunes. The airline rose from the bottom to the top of federal rankings for on-time performance and profits followed. Having made a loss in excess of $100 million in the year prior to the takeover, Continental reported a profit of over $700 million in 1997.

Five years after agreeing the deal, Bonderman and his investors sold their stake to Northwest Airlines for an 11x return.

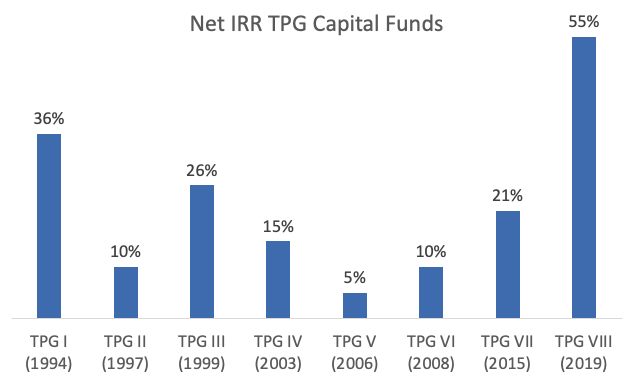

The deal established Bodmerman and Coulter’s credentials, giving them the taste for more. To do the Continental deal, they’d set up a special purpose vehicle; to do something more durable they’d need a firm. Bonderman was based out of Fort Worth, Texas and Coulter out of California, so they called their new firm Texas Pacific Group (TPG). In 1994, they went out to raise their first fund, targeting $500 million. Compared to other firms, it was a modest ask; Blackstone was out raising its second fund of $1.4 billion, and KKR was on its seventh, its fund sized at close to $2 billion. In the end, Bonderman, Coulter and a third founding partner, William Price, closed their fund with $720 million of commitments. Their pitch to investors was that it would be deployed in “complex transactions, focusing on industries undergoing change, and applying cautious contrarianism.”

2. J Crew

An overview of TPG’s early days doesn’t have to include an analysis of J Crew. Burger King would do. Or Del Monte Foods. Or Ducati Motorcycles. In the years that followed that first fundraise, TPG mounted plenty of corporate buyouts. The first fund returned investors 4.4x their money. A second fund, in 1997, returned investors 2.0x; and a third fund (1999) returned them 3.3x.

But J Crew has a special place in the history of TPG – the firm bought it twice.

TPG first acquired a stake in J Crew back in 1997. It was a huge brand, still managed by its founding family, but it lagged peers like Eddie Bauer in mail order and Banana Republic in physical retail (these were the days before e-commerce!). TPG put together a deal worth $560 million to buy 88% of the company, throwing in $190 million of cash alongside some other private equity buyers, and raising debt to fund the rest.

On the strength of its Continental investment, TPG developed a reputation less as a slash-and-burn financial engineer and more as an operations expert that could fix and grow underperforming assets. To this day, TPG is proud of its operating expertise. It was one of the first private equity firms to establish an in-house operations group – currently staffed with 50 professionals – and it views the function as a source of competitive advantage.

But it took a while for it to get a grip on J Crew. The first CEO hired by TPG resigned after a year and the second oversaw falling sales. The third did better, slowing down the opening of new stores but bond investors remained nervous. It wasn’t until the fourth CEO was installed, in 2003, that performance really started to improve.

Mickey Drexler was recruited from GAP, invested $10 million of his own money in the business and got to work. By the end of 2004, operating revenues turned positive and losses were cut almost in half. Unlike his predecessors, Drexler raised prices and quality and resisted steep discounting.

In 2006, TPG took J Crew public at $20 a share while retaining its stake. The company continued to do well. In 2007, revenues reached $1.3 billion, up from $600 million in the year before TPG bought it. In 2008, Michelle Obama famously wore J Crew in an appearance on The Tonight Show with Jay Leno and went on to wear its clothing frequently on state trips as first lady.

As soon as its lockup expired, TPG began to sell. Between 2007 and 2008, it sold most of its shares at prices between $33 and $44, finally disposing of its final shares in April 2009 at $14. All told, TPG made a 7x return on its investment.

And then it bought it back.

TPG had got to know J Crew’s business well, and James Coulter had remained on the board. With its stock price depressed, the firm decided to have another crack. In 2010, it teamed up with another private equity firm to buy it back for $43.50 a share, a ~30% premium to where the stock was trading in the market.

This time, the trade wasn’t quite so successful. First, some shareholders questioned the cosy relationship between TPG and J Crew’s CEO, Mickey Drexler. They argued that Drexler conspired with Coulter to prevent other interested parties from bidding for the company. A lawsuit was eventually settled for $16 million.

Then, J Crew found itself on the wrong side of changing fashion, as the company lost share to brands like Zara and H&M. It suffered a loss in 2014, and sales continued to drop from 2015 to 2017.

Finally, the company’s leveraged balance sheet took its toll. J Crew had $50 million of debt on its balance sheet in 2010, prior to TPG’s second takeover; by February 2020, it had $1.7 billion of debt. In May 2020, the streets quiet from lockdown, J Crew filed for bankruptcy protection.

Not that TPG lost much money on the trade. Over the duration of its ownership, J Crew paid out $682 million in dividends. It also paid its private equity owners annual “monitoring fees” and an initial transaction fee of $35 million. Such fees are a feature of the traditional private equity revenue model. In the first nine months of 2021, TPG booked $80 million of monitoring and transaction fees. While they fade into insignificance next to the scale of performance fees, they represent a recurring income stream uncorrelated to underlying portfolio performance.

3. Washington Mutual

Most bank investors know money can be made recapitalising failed banks. The trick is to make sure all bad loans have been recognised. If they time it properly, new investors can benefit from recoveries and write-backs, dodging the credit losses meted out to legacy investors.

David Bonderman was aware of the playbook. In the late 1980s, he’d helped Robert Bass buy American Savings and Loan, one of the country's largest thrifts, from the federal government which had taken it into receivership after catastrophic losses. He presided over the liquidation of billions of dollars of assets and orchestrated the thrift’s recovery, eventually selling it to Washington Mutual for a $750 million profit.

So when Washington Mutual hit problems of its own in 2007, Bonderman was interested.

At the beginning of 2008, Washington Mutual needed to raise capital to plug losses in its mortgage book. It had already raised some, in the form of preferred stock, a few months earlier, but as the market deteriorated, it became plain it hadn’t been enough. Management estimated that losses in their home loan portfolio would spiral to between $12 and $19 billion, on which basis they would need at least $4bn additional capital to avoid breaching regulatory thresholds. They pitched investors.

Four investor groups stepped forward – TPG, Cerberus, Blackstone and JPMorgan (which wanted to buy the whole bank). After comparing their offers, Washington Mutual management chose TPG. The TPG team was more conservative than Washington Mutual management on potential future losses – they projected losses in the mid $20 billions – and their offer reflected that. They proposed a $2 billion capital injection, of which TPG would contribute $1.35 billion and a small group of co-investors the rest, at a price of $8.75 per share, a 20% discount to where the bank’s stock was trading at the time. With TPG as an anchor, the bank would be able to raise a further $5 billion from public investors. Bonderman was appointed to the board. To mitigate its risk, TPG was offered warrants and a “price reset” feature which meant that TPG would be compensated if Washington Mutual were to raise another round of capital in the future at a lower price. 1

Washington Mutual never did raise another round because within six months it was bust. It continued to rack up losses and increasingly had to contend with deposit outflows, putting its liquidity profile in jeopardy. Once Lehman collapsed, there was no hope. In the ten days after, depositors pulled out $17 billion of funds. Regulators normally wait until Friday to close failing banks to give them the weekend to sort things out. The run on Washington Mutual was so intense, regulators closed it on Thursday, September 25th while its CEO was in transit between New York and Seattle.

TPG wrote a letter to its investors:

We have been successfully investing in regulated industries since 1986. Over this time we have seen moments of turmoil in industries as far flung as airlines, health insurance and Asian banks. However, in all this experience, we have never run across a situation where the combination of regulatory uncertainty and market disruption have combined to swiftly and decisively overtake the fundamental aspects of an investment.

It’s very unusual for private equity firms to lose money as quickly as TPG did on Washington Mutual. Usually they have some agency over the process. Indeed, they benefit from the luxury of locked-up capital – not subject to redemption – which gives them discretion to time exits according to market conditions. While investors may be keen to maximise rates of return, private equity firms get paid on a multiple of investment (notwithstanding a compounding hurdle rate, in TPG’s case, 8%) so they can afford to be patient.

Usually, when a loss does occur, it crystallises over a much longer period than six months, like it did in the case of J Crew take two. Unfortunately for TPG, it deployed large pools of capital into the teeth of the financial crisis, and losses subsequently emerged. Its fifth private equity fund, raised in 2006, returned 1.4x to investors, a net rate of return of just 5%. Its sixth fund, raised in 2008, returned 1.8x, equivalent to a 10% return.

As well as harbouring J Crew and Washington Mutual, these funds were dragged down by another loss-maker: Caesars.

4. Caesars

In 2006, David Bonderman was introduced to the CEO of Caesars by a mutual friend with whom he’d worked at Bass. Caesars, known at the time as Harrah’s, was a leading gaming and lodging company with strong brands including both Caesars and Harrah’s, Horseshoe, and World Series of Poker. Bonderman sensed an opportunity. The company maintained a loyalty programme that brought in repeat customers. Its value, combined with potential cost savings, convinced him to make a bid for the whole company. He paired up with Apollo, and the two firms mounted a leveraged buyout

It was one of the biggest leveraged buyouts to date. The total purchase price was $30.9 billion. TPG and Apollo put in $1.325 billion a piece, co-investors contributed $3.4 billion, and the rest was raised in debt.

The two private equity firms forecast that Caesar’s enterprise value could reach as high as $40 billion by 2012, boosting the value of their equity investment from $6 billion to between $15 and $20 billion. Even though winds of recession were beginning to blow through Las Vegas as the deal reached completion in January 2008, the firms considered Caesars to be close to recession-proof.

Unfortunately, that was a misplaced assumption. In 2008, operating profit at Caesars was already down a third from 2007. Between 2007 and 2009, overall visitors to Las Vegas fell by nearly 7% but gambling revenue fell by close to 20%.

Max Frumes and Sujeet Indap pick up the story in their book, The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall Street. They detail how the two firms tried to protect an investment that was going increasingly awry:

The monumental task of turning Harrah’s around was going to require all of the tools available across TPG and Apollo, each a master of different domains. TPG, which resurrected Continental Airlines, focused on the so-called “left side of the balance sheet” where the company’s physical assets were enumerated. Its operational expertise could be used to make Harrah’s leaner and meaner. Apollo, its core strength in financial engineering, would take on the right side of the balance sheet, where the liabilities and equity details of the company were listed.

The firms tried to eke out some efficiencies, but they weren’t sufficient to offset the drop in revenues. TPG operations professionals even followed housekeepers around the hotels to track how they cleaned a floor of rooms. (They identified inefficiencies in the demanding physical task of removing bed sheets and so installed “strippers” to run ahead of the housekeepers stripping bed sheets.) Meanwhile, interest payments remained stubbornly close to $2 billion a year, beginning to exceed the company’s cash generation. Rather than bed stripping, the company’s owners had to resort to asset stripping: a full-on balance sheet restructuring was required.

This is where the firms got a bit too clever. Between 2011 and 2014, they engaged in a number of financial transactions, shifting assets away from the legal entity that housed most of the debt. Caesars, Apollo and TPG were effectively on both sides of these deals, selling assets between each other. As Caesars approached bankruptcy, these transactions gave rise to a series of lawsuits. On the one side, TPG and Apollo; on the other, Caesar’s debtholders, which included some of the largest hedge funds in the industry.

As Frumes and Indap tell it, by now TPG had taken something of a back seat. They cite a report compiled by Richard Davis, the bankruptcy examiner:

One key subtext of the report was just how much Apollo had taken over Caesars. TPG had largely ceded the financial functions to Rowan and Sambur [Apollo executives]. Davis did not care much for David Bonderman, the TPG co-founder, after interviewing him. Davis found him to be like an eccentric uncle who was not sharp on the details surrounding Caesars.

When the dust settled on the case, TPG and Apollo walked away with some equity in the restructured business, albeit diluted down. Unlike Washington Mutual, this wasn’t a zero; it also had a silver lining:

5. Uber

Unusually for a buyout firm, TPG was early to get into growth equity. The company credits its roots in San Francisco for that, but Bonderman’s personal brand may also have had something to do with it. When Uber was raising money in 2013, founder Travis Kalanick wanted to bring TPG into the round. Mike Isaac writes in his book, Super Pumped: The Battle for Uber:

Kalanick wanted the swagger and global connections that came with taking money from TPG Capital. The firm also offered him a trip on its corporate jet, a creature comfort that came with only top-tier firms… A legend in private equity, Bonderman was a founding partner at TPG who harbored connections with celebrities, executives, regulators, and heads of state around the world… Bonderman’s participation telegraphed Uber’s importance to the broader business community.

TPG got a very good deal on Uber, buying $88 million worth of shares from co-founder Garrett Camp at a discount. Bonderman took a seat on the board from where he influenced Uber’s exit from China and the ultimate ousting of Kalanick. By the time Uber IPO’d in 2019, TPG had made around a 20x return on its investment.

Since raising its first growth equity fund in 2007, TPG has invested $15 billion in growth equity, about a fifth of what it has invested in traditional private equity. As well as Uber, high profile deals include AirBnB and Spotify. Its returns have been pretty good – 1.9x as at end September 2021, compared with 2.0x across private equity – although most of them are still unrealised. Of the total cumulative value created in growth, 57% is still unrealised, compared with 22% in traditional private equity.

The Next Trades

TPG has largely recovered from some of the bad trades it did prior to the financial crisis. It laid low for several years, not raising a buyout fund at all between 2008 and 2015. Since then, it has picked up the pace, rapidly accelerating its rate of capital raising and capital deployment. Around 45% of its $109 billion of assets under management is attributable to funds raised since 2018. These include some impact funds, where TPG is a market leader (and Bono a partner).

Compared with public peers, though, TPG’s financial structure is still old-school. Unlike them, it hasn’t accumulated permanent capital, a theme we discussed in Other People’s Money. The firm’s preferred model is to go out and raise a fund, deploy it and distribute gains to investors, keeping a 20% carry for itself (beyond a hurdle rate of 8%). Along the way, it generates management fees (and monitoring fees, and transaction fees) at a rate of 1.45% which compares favourably with peers whose average is 1.05%.

The IPO is being structured such that most of the management and other fees drop down for outside shareholders. While they will be used to cover salaries and admin costs, they won’t be used to cover partner bonuses. The margin on those fee earnings is currently 37% but the company reckons that can expand as it scales up new funds. Fund sizes have lagged those of peers since the firm’s early days, so there may be an opportunity to step up fund sizes.

In addition, 20% of performance fees are being promised to outside shareholders. The skew creates a structure which is weighted more towards fee earnings than many peers, but that’s because of the way spoils are shared with partners rather than anything fundamental to the core business.

Of TPG’s 640 lifetime trades, around 280 are currently live. Right now, unrealised values reflect outcomes closer to Continental, Uber and J Crew I. But if the market turns, then WaMu, Caesars and J Crew II provide a cautionary tale.