Welcome to another issue of Net Interest, where I distil 25+ years of experience analysing and investing in financial stocks into a weekly newsletter. This week’s topic is Brookfield Asset Management, one of the most interesting companies in Canada. Once a conglomerate, it has spent 20 years transitioning into a large investment management firm. Next week, the metamorphosis will be complete when it spins off its asset management business onto the Toronto and New York stock exchanges. Paying subscribers get some extra goodies, too — please consider joining them by clicking here. Thanks!

“Private-equity funds are the conglomerates of this era.” — Jeff Immelt

One of the first stocks I ever bought was a UK-listed share called Trafalgar House. It was the early 1990s, many years before I would begin managing money professionally, and I was still learning my way around the stock market. Based on the rudimentary analysis I did, the stock looked cheap – but then it would have done: Trafalgar House was a conglomerate. And as I would later learn, conglomerates almost always look cheap.

Conglomerates became fashionable during the 1960s. Their growth stemmed from three sources. First, strict enforcement of antitrust regulations made it harder for companies to combine within industries, so managers looked outwards to satisfy expansionary ambitions. Second, lax accounting rules allowed acquisitive companies to post deceptively high growth rates, easing their access to capital markets to fund further growth. And third, business studies was emerging as an academic discipline and with it the notion that general management skill could be applied across different sectors. In the ten years after 1965, some 80% of all merger and acquisition activity in the US involved conglomerates.

It was against this backdrop that Trafalgar House was born. The company was floated on the London Stock Exchange in 1963, initially as a property developer before it embarked on a multi-year acquisition spree that saw it pick up businesses across hospitality, property, housebuilding, shipping, construction and engineering. Among its assets: the storied Ritz Hotel and the Cunard shipping line.

But the company came unstuck in the recession of 1990. Having overexpanded in the years prior, it was forced to write down the value of several of its assets, increasing the burden on its debt. The financial problems also exposed underlying operating problems: Acquisitions were never properly integrated and as a result costs remained high, management controls were scant and information flowing to the centre was suspect. “The group went round making acquisitions that were not bedded in,” said one analyst at the time. “You had a lot of businesses that were really fiefdoms, independent operations.”

It was just after this that I got involved. Mismanagement aside, the company had some attractive assets and as a portfolio they appeared to be worth more than the Trafalgar House stock price suggested. Sadly, I never got to see that valuation gap crystallised. The company was taken over by a Norwegian industrial group in 1996 for £904 million and I just about made my money back. It was a lesson in the vagaries of valuing a conglomerate.

Trafalgar House was not the only conglomerate to stumble. Over the 1980s and into the 1990s, many were unwound. It turns out few managers have the skills to steer businesses simultaneously across disparate sectors, and extra layers of management increase costs. In addition, investors came to realise that they can effect diversification directly, via portfolio construction, without needing to rely on a company to do it for them. In the US, conglomerates like Litton Industries and ITT preceded Trafalgar House to the wall.

In Canada, however, one conglomerate thrived through reinvention. Once one of the largest companies in the country, it employed more than 110,000 Canadians and constituted 15% of the Toronto Stock Exchange. Like Trafalgar House, it faced collapse in the wake of the 1990 recession but, unlike Trafalgar House, it restructured and is still around today. That company is Brookfield Asset Management. Next week, it completes its restructuring by spinning off an asset management business that it has been cultivating alongside its agglomerated businesses for 20 years.

From Edper to Brascan to Brookfield

By all accounts, Sam Bronfman was a domineering entrepreneur. He navigated Prohibition in the US to grow his family’s Montreal-based distillery business, Seagram, into one of the largest in the world, producing brands such as Chivas Regal, Mumms and Martell. But having initially set the business up alongside his brothers, he later sought to cut them out. “The business is mine,” he told his brother Allan, a vice-president and director in the business. “You must understand that the words ‘we’ and ‘us’ no longer apply.”

In the early 1960s, Sam forced Allan to sell him the Seagram shares that Allan had placed in trust for his children for a consideration of $16 million. By then, Allan’s children, Edward and Peter, were in their early 30s and, eager to make a go of it themselves, used the proceeds to seed their own investment business. The business, called Edper as a portmanteau of their names, made its first major independent investment in 1969. Sam was so jealous, he threw Edward and Peter out of his offices.

Over the next twenty years, Edper grew into a giant conglomerate. By 1990, the Edper empire controlled 32 public companies and hundreds of private companies. Its holdings included Trizec (North America’s largest publicly traded developer), Royal LePage (Canada’s largest real-estate brokerage), John Labatt (Canada’s second largest brewer), Noranda (a C$10 billion natural resources giant), Noranda Forest and MacMillan Bloedel (leaders in paper products), and London Life (Canada’s largest insurer). Some of these businesses were held via a holding company, Brascan, which also maintained power and transportation interests in Brazil. (Brascan is a portmanteau of Brasil and Canada; they like portmanteaus in Canada.)

Steering Edper’s growth was a man called Jack Cockwell, a South African accountant whom Edward and Peter had hired when he was still in his twenties. Cockwell perfected various strategies to obtain control of companies while minimising the amount of capital the firm needed to deploy. One strategy was to take a controlling stake in a public company that would take a controlling stake in another public company that would take a controlling stake in yet another, so that Edper could exercise control with a relatively small holding in the underlying company. Cockwell called this the “cascading effect of leverage”.

Other strategies included cross-ownership or partial ownership of a parent company by its subsidiary, and the use of restricted or non-voting shares for public investors with super-voting shares being retained for insiders. Together, the strategies enabled Edper to control billions of dollars of assets without having to use much of its own money.

A newspaper story from 1990 provides a worked example:

“The process worked along these lines: Hees International, the group’s Toronto-based merchant banker, would handle the issue of Cdollars 100m worth of shares in an Edper company, half of which would be bought by Edper and the other half sold to the public. Hees would then take the dollars 100m proceeds and invest it in a dollars 200m share issue of a subsidiary of the first company, with the public again picking up half. That process, repeated five times, turns Cdollars 50m into Cdollars 1.2bn. In other words, a Bronfman-controlled company picks up Cdollars 1.2bn and yet Edper puts up only 3.125 percent of it.”

The upshot is that while Edper maintained control of its subsidiaries, its effective equity interest in those at the bottom of the pyramid was small. According to the 1991 Hees annual report, Edper’s equity interest in a range of large subsidiaries was no more than 13%. To get there, Edper companies issued more securities than anyone else in Canada during the 1980s, raising more than C$30 billion in equity.

The result was a complex corporate web. So dizzying was the structure that the Globe and Mail once likened investing in Edper to watching a basketball game in the dark:

“Shareholder-spectators know there is a game going on because they can hear the ball bouncing and feet scuffling on the floor; they just can’t see what’s happening… But there is a big electronic board overhead that periodically flashes the score so spectators can see how their team is doing. Chief strategist Jack Cockwell and his team of crackerjack lawyers, accountants and bankers tell their shareholders ahead of time what the score will be. They believe the audience should be satisfied as long as the numbers match up to what the managers promised.”

In 1990, the structure began to splinter. The global recession that hit Trafalgar House in the UK also sent shockwaves through Canada. Companies within the Edper group were very highly leveraged, in some cases having used equity stakes in other Edper companies as collateral. As stock prices fell, debt levels became exposed. Debt backed by hard assets such as property proved no safer, as commercial real estate values also fell. Analysts estimate there may have been between C$30 billion and C$50 billion of debt in the group, serviced by dividends that flowed from subsidiaries up to the parent company. Having listed the ultimate parent company, Edper Enterprises, in 1989, Cockwell and the Bronfman brothers saw the value of its equity decline by 90%.

The company rushed to deleverage. In a single week in February 1993, management sold off stakes in Labatt and pulp and paper giant MacMillan Bloedel in what Canadian business reporters took to calling “the great Edper lawn sale”. All told, between 1991 and 1993 the Edper companies raised more than C$9 billion through share issues, asset sales and debt financing.

At the end of it, in 1995, the Bronfman brothers exited the business, leaving Cockwell as the main shareholder. Cockwell folded the remaining assets into Brascan and organised the business around three key divisions: real estate (from Trizec), power (from Brascan), and financial services (formerly Trilon). He also hired a young accountant of his own, Bruce Flatt. Flatt joined the firm in 1990 at the age of 25, became chief executive of the real estate business in 2000 and took over from Cockwell as chief executive of the now renamed parent company, Brookfield Asset Management, in 2002.

The New Conglomerates

As the conglomerate model of financial capitalism waned, another model took hold. Private equity buyouts gained momentum throughout the 1980s, spearheaded by firms like KKR and Blackstone. Initially, private equity firms made a lot of money dismantling conglomerates, using leveraged buyouts to pick up “orphan assets” from failing conglomerate organisations. Yet although buyouts occurred as individual events, they were typically carried out by the same firms, the same partners, and housed in the same portfolios. Over time, those firms and portfolios got large enough that they now resemble the conglomerates of old.

Take Blackstone. As of mid-2021, the firm controlled 250 companies across a range of industries, in aggregate employing more than half a million people. There are differences between Blackstone and a conglomerate, of course. Each of Blackstone’s constituent companies is organised and funded by a separate investment partnership and remains independent of the other companies’ operations. And while a conglomerate is organised as a perpetual corporation, private equity funds typically have a limited life (say, 12 years) at the end of which they have to sell their investments and return capital to fund investors.

But there are similarities, too. Blackstone runs a “portfolio operations” team to provide functional support across its portfolio companies, helping company management across areas such as procurement, healthcare and data science. At the time of its investor day in 2018, the Blackstone team comprised 36 professionals plus 35 external advisors and had delivered $600 million of savings in the last full year. These are exactly the kind of “synergies” originally promised by conglomerates.

Private equity firms’ own capital commitment to deals has also increased over the years. While initially the private equity model centred on investing other people’s money, firms now allocate their own capital more extensively. KKR deployed an average of $2.4 billion per year of its own capital in investments in the four years through 2020, up from $1.5 billion in the four years prior. Apollo’s CEO, Marc Rowan, has likened his balance sheet intensive model to the ultimate successful conglomerate – Berkshire Hathaway.

In some ways, the conglomerate model and the private equity model are converging. Yet while in most cases it’s the traditional private equity model that’s encroaching on conglomerate turf, at Brookfield it is the other way around.

“We had our own money invested in our own businesses and over time we figured out which ones we like,” Bruce Flatt said in a recent interview. “And then we raised money around those businesses… And then decided that the way that we could fund businesses without taking undue risk was to start partnering with clients, with institutions. And eventually we brought institutions into deals and eventually we did what many other private equity firms were doing which was raise funds.”

The Flatt Years

Taking control of Brookfield’s predecessor, Brascan, in 2002, Flatt “continued to narrow the areas where we operate, while at the same time, broadening our activities within each of these areas.” He sold off the cyclical mining interests the group owned while retaining the infrastructure assets that had been built around them. He also launched investment funds to attract external capital. By the end of 2003, the firm had $5 billion assets under management across five funds, including $1.2 billion seeded by Brascan itself. Today, the firm has over $750 billion of assets under management, of which $407 billion are fee-earning, drawn in from around 2,100 institutional investors globally.

Flatt articulated his business strategy as being “to own, manage and build businesses which generate sustainable free cash flows.” His key performance targets were annual growth in cash flow per share of 15% and a long-term goal of 20% cash return on equity.

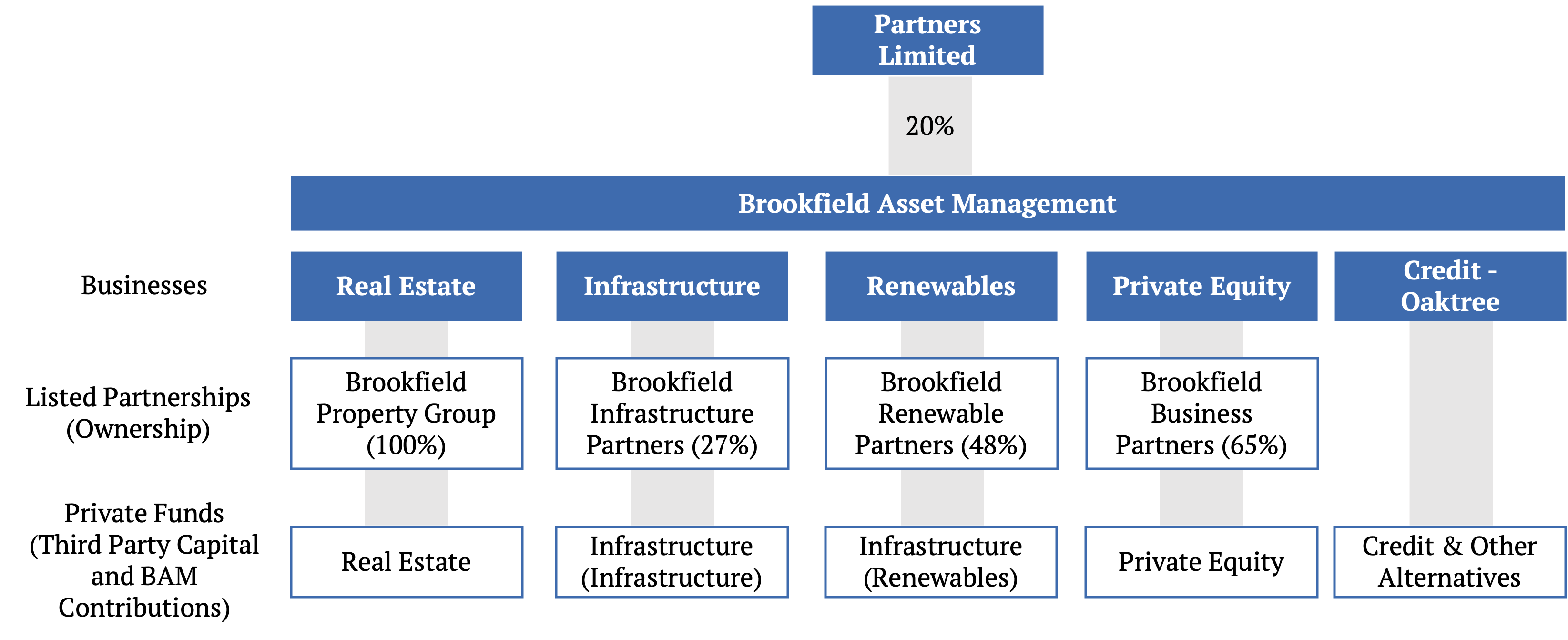

Although he was intent on steering the group in a new direction, he continued to borrow from many of the strategies devised by Jack Cockwell, who stayed on as chairman throughout. Rather than float individual businesses, though, he grouped assets into silos and floated them as listed partnerships on the Toronto and New York Stock Exchanges. Over time, the firm spun off stakes in Brookfield Property Partners, Brookfield Infrastructure Partners, Brookfield Renewable Partners and Brookfield Business Partners. These entities represent permanent capital vehicles, allowing other investors to participate in their underlying assets as direct shareholders. But as the manager of these entities, Brookfield levies fees, meaning it is able to extract a share of their cash flows disproportionate to its equity holding.

Flatt also concentrated control of the entire group in the hands of a few partners. An entity called Partners Limited, controlled by Flatt, Cockwell and around 40 others, owns 20% of Brookfield but retains special voting rights and has the power to appoint nine out of the group’s 16 directors. Partners is a legacy of the Bronfman days, “formed in 1987 to provide the senior group managers with a financing vehicle to pool their resources and thereby become a financial partner with Peter Bronfman in the control of the Edper group.”

Another trick he has carried through from the Cockwell days is communicating the “the score” on “the big electronic board overhead”. Cognisant of the complexity of his operations, Flatt regularly tells investors what he thinks the group is worth. He calls it the firm’s “plan value”. Back in 2002 when he became CEO, he estimates the “plan value” was $4 a share. He now pins it at $82-94 per share. Looking out to 2027, he counsels investors that it should hit $175-198.

While these strategies may be unusual in the world of conglomerates, they are less unusual in the world of private equity. The listed partnerships are analogous to funds, with the benefit that they are permanent – indeed, as we have discussed here before, permanent capital has become a more widespread theme within the industry. And by owning so much Brookfield stock, management interests are aligned. In his 2012 letter to shareholders, Flatt wrote: “[Senior management is] commit[ed] to align our interests with yours by holding the vast majority of our individual net worth in Brookfield equity.”

Since taking over as CEO twenty years ago, Flatt has delivered compound returns of 19% per annum for shareholders. This is slightly ahead of the growth in “plan value” of 16% per annum plus a dividend yield of 2% as a result of some multiple expansion along the way. There are several reasons for the success.

First, Brookfield benefited from clear tailwinds. The group’s focus is “long life” assets like infrastructure and real estate which performed well when interest rates fell. It raises the question how those assets will perform now that rates are backing up. The company argues that its assets provide inflation protection, but management also thinks/hopes that “as inflation abates…interest rates will slowly come down, but this might take some time, depending on how long it takes to harness inflation.” Its real estate business is particularly exposed, although it no longer gets the transparency of its own listed partnership – last year, Brookfield bought in the share of Brookfield Property Partners it didn’t own at a 25% discount to carrying value.

Second, Brookfield has managed risk well. Learning from the near collapse of Edper, the company employs a series of strategies to reduce risk. It preserves a high level of liquidity and matches “liquidity and duration of the assets and operations being financed” to debt characteristics. Debt typically has recourse only to a specific asset, even if it is more expensive than cross-collateralized finance. As a result, during the global financial crisis, “we did not have to face the major issues which a number of others have had to.” The firm currently carries $11 billion of long-term debt on $79 billion of equity, and has $70 billion of cash and semi-liquid investments on hand.

Third, the firm buys well, embracing a “value investing” mindset in its approach to investments. Flatt emphasises the importance of “purchas[ing] assets at a discount to their replacement cost, building a margin of safety into our acquisitions.” Flatt himself made his mark overseeing the acquisition of a 1.2 million square foot interest in Three World Financial Centre at a substantial discount to replacement value in the immediate aftermath of 9/11. The firm subsequently went on a shopping spree for $4.1 billion of investment during the tail end of the global financial crisis, and bought “various distressed real estate and infrastructure investments” in Europe during the sovereign debt crisis. “We keep this picture in the office to remind our people that one should always look for opportunity away from where the crowd is going,” says Flatt:

Finally, size became a competitive advantage in the asset classes Brookfield is active in, unlike in public market investing (as we discussed in Zuckerman’s Curse and the Economics of Fund Management):

“We are often asked why we do not have the same issues that some public equity managers have investing funds as they grow larger. The difference is that infrastructure (as well as real estate and private equity) usually becomes more attractive as investments get larger. The competition for larger acquisitions is less and the sophistication required to operate these assets increases because of their complexity, therefore favoring large and experienced managers. Lastly, the larger assets acquired are generally also higher quality – they often have better counterparties, and stronger management teams.” (Brookfield Asset Management Letter to Shareholders, 2018 Q4)

Brookfield Today

Even though Bruce Flatt works hard to communicate his firm’s “plan value”, investors are not always convinced. Questions persist as to whether Brookfield is a conglomerate or an asset manager. Over the years, the market-implied value of the asset management component has fluctuated wildly.

As a result, Brookfield is finally spinning out its asset manager. Next week, shareholders will receive one share in a new company, Brookfield Asset Management Ltd (BAM) for every four shares they currently own in the holding company, which will be renamed Brookfield Corporation (BN). It’s not entirely a clean break though. The holding company will retain a 75% interest in the manager, and will also continue to extract fees. Although the asset management company will retain 100% of its fee-related earnings, all of the carried interest on existing funds and a third of gross carried interest earned on new funds will stay with the holding company.

Shareholders in the Corporation therefore have exposure to three platforms:

The “conglomerate”. The firm carries around $60 billion of equity exposure on its own balance sheet – $11 billion in renewable power and transition; $8 billion in infrastructure; $4 billion in private equity; and $35 billion in real estate. Going forward, it will also count its stake in the asset management business. These assets currently generate around $2 billion of annual distributions.

The “asset manager” has over $400 billion of fee-earning assets. Brookfield reckons this can grow to $1 trillion. The manager currently throws off fee-related earnings of close to $2 billion per year, which the company projects will grow to $4.3 billion by 2027; by then, some carried interest may be kicking in, too.

In addition, the firm has an emerging insurance business. It currently has $10 billion of equity invested in it on $40 billion of assets. The company reckons it can grow those assets to $400 billion.

It’s too late for Trafalgar House, but the shift from conglomerate to asset manager is a neat one. Following the spin next week, we’ll learn if it’s enough to banish the discount.

For more on Brookfield, Colossus recently released a ‘Business Breakdown’ of the company, which includes plenty of additional resources. Brookfield’s September investor day presentation is also useful reading. In addition, Austin Value Capital has a compilation of letters, annual reports, investor day presentations and annual supplements of Brookfield and its associated companies on their website. Finally, Manual of Ideas members might like Alex Gilchrist’s ‘A Profile in Leadership: Bruce Flatt, CEO of Brookfield Asset Management’.