The Cautionary Tale of Equity Research

Plus: Chinese Retail Investors, Gold Financing, Monzo

Issue #11 of Net Interest and welcome to 162 new subscribers, especially those from London Business School who are part of a referral programme to raise money for the school. Every Friday I distil 25 years of experience looking at financial institutions into an email that explores key themes trending in the industry. If you’re reading this, but haven’t yet subscribed, sign up here to receive Net Interest fresh into your inbox every week:

The Cautionary Tale of Equity Research

We’ve all heard of doctors who neglect their own health; financial advisors whose personal finances are a mess. Well, research analysts suffer from the same phenomenon. Their job is to value businesses, yet they struggle to value their own.

After a career spent as a research analyst, I turn my sights on my former industry. This note explores the value of equity research. It touches on price bundling, on principal agent dynamics and on the unintended consequences of regulation. So really it’s about much more than equity research.

But let’s start at the beginning.

Twenty five years ago I stepped out onto the trading floor of my bank in the City of London, a newly minted equity analyst. The job entailed hoarding industry knowledge in a sector and making stock recommendations on the companies within it. I spent hours studying the industry, building company models, questioning management, cultivating contacts, monitoring share prices. The end-product would be a carefully crafted research report with a simple punchline—buy or sell a company’s stock. I would present the research report to the bank’s sales force from a podium at the front of a cavernous trading floor.

And then, just before the opening bell, they would…give it away for free.

They would fax it, mail it and precis it to everyone they knew. (Technically they would send it to their clients but their clients were everyone’s clients – no exclusivity here – and they’d send it to potential clients, too. So basically, everyone.)

To understand why they did this we need to go back a generation to the 1960’s and 1970’s when equity research emerged as a credible profession. In those days brokerage commissions were fixed by law and so brokers couldn’t compete on price. Instead they offered other services and equity research emerged as the big one (alongside fine dinners and Wimbledon tickets).

Even after brokerage commissions were deregulated, the practice stuck and equity research became part of a bundled product that was offered to institutional investors—buy some equity trade execution and get some equity research thrown in for free.

In many ways the equity research industry behaved like the newspaper industry:

There is clearly an investigative component to the job. One firm I know even had Bob Woodward come in to speak to its analysts.

Just like journalists, many of the best analysts I ever worked with are history graduates. They’re good at distilling information for signal, and they’re not bad at crafting a narrative around it.

Both models package together a broad range of content—oil and gas research is distributed alongside tech research in the way that politics news is distributed alongside sports news. Investment banks used to talk about their ‘waterfront coverage model’; newspapers took it as read.

Both businesses have had to adapt to falling information costs. Equity research had to adapt earlier because its customers gained access to alternative information sources before they got cheap enough to attract newspaper readers. This led to a bifurcation of content between ‘quality’ and ‘quantity’.

Both models compete for engagement. Equity research incentives are structured to encourage click throughs to trade execution. This means that within the bifurcation, quantity often wins out.

There is one difference between the business models though. Whereas there are three participants in the newspaper model – editorial, advertisers and readers – in the case of equity research the readers and the fee-payers are the same—institutional investors, who pay for one thing and get the other for free.

This should have eliminated any conflict of interest. Unfortunately it didn’t.

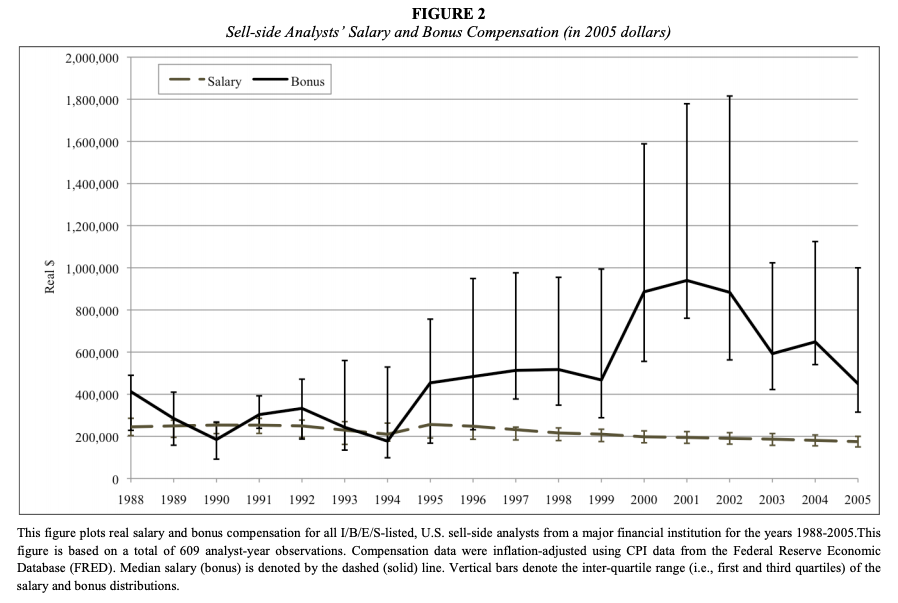

Since being deregulated in the US in 1975, brokerage commissions had been falling. Between 1980 and 2000 they fell from around 1.0% of the value of stock traded to around 0.20%. This wasn’t devastating to brokerage firms because lower price drove higher demand, and trading volumes rose (a dynamic that has continued to the present day). But it wasn’t especially conducive to growth.

In the late 1990’s a new revenue stream emerged that was able to provide some growth—initial public offerings (IPOs). The market for IPOs was booming and their margins were high. Companies going through IPO would pay investment banks a fee of around 7% to get them to market. Equity research latched on—analysts became marketing personnel not just for their banks’ trading businesses, but for their IPO and other equity underwriting businesses too.

No-one personifies this era of equity research more than Jack Grubman. Grubman was the telecom analyst at Salomon Smith Barney (part of Citigroup). He understood the revenue upside from banking even if it meant putting Buy recommendations on stocks like Focal Communications:

“If I so much as hear one more fucking peep out of them we will put the proper rating (ie 4 not even 3) on this stock which every single smart buysider feels is going to zero. We lose credibility on MCLD and XO because we support pigs like Focal.”

(Unfortunately for Grubman he was active in that window of time after the introduction of email but before even telecom analysts realised it leaves a permanent record.)

Grubman famously upgraded his recommendation on AT&T from Hold to Buy in November 1999 after his boss, who was also a non-executive director of AT&T, suggested that he take a “fresh look” at the stock. Salomon Smith Barney went on to win US$63 million in investment banking fees from the IPO of AT&T’s wireless unit and Grubman got his kids into preschool. He also got paid very well for his efforts—between 1999 and August 2002, when he left the firm, Grubman's total compensation exceeded US$67.5 million.

This construct, of allowing investment banking to support equity research, was eventually dismantled after an investigation spearheaded by New York’s Attorney General, Eliot Spitzer. But not before it altered the economics of the industry.

Grubman wasn’t the only one to see his compensation rise. Analyst pay rose across the industry, although not uniformly. The variance of pay increased as ‘superstar’ dynamics took root. Analysts like Grubman were able to leverage their personal brand to extract a greater share of the value they helped create. In the three years between 1999 and 2001 Salomon Smith Barney earned more than US$790 million in gross investment banking fees from telecom companies covered by Grubman. He took home ~6% of that.

(Source: here)

The model also fuelled an oversupply of equity research. Most large banks tried to cover as wide a range of stocks and sectors as possible in an effort to win investment banking business. As a result, many stocks were covered by more than 100 analysts. I remember John Mack, then CEO of Credit Suisse previewing a round of cost cuts after the bubble had burst in 2001 by asking a roomful of analysts why so many of them needed to follow his stock. (I was one of them.)

After Spitzer, equity research went through a readjustment phase. It was a cost centre in search of a revenue stream, wandering around like an orphan looking for a kindly parent to adopt it. Proprietary trading briefly stepped up to fill the role – analysts would submit their ideas to internal hedge funds for a share of the returns – but the Volcker Rule established in the aftermath of the financial crisis killed that off.

So equity research went back to its roots as a product bundled together with trading commissions.

It made some sense. As a stand-alone product, equity research is very difficult to value. It’s hard to keep private, so clients are reluctant to pay for it. And the range of values they assign to it can be huge. As an investor later in my career, I would read a lot of guff, but occasionally I would read research of tremendous value which directly contributed to millions of dollars of investment performance (although knowing which was which ex ante is a challenge).

Hence bundling. Bundling works best when two conditions are met: high variance in demand and zero marginal cost. The first makes the product difficult to price on a stand-alone basis; the second ensures it’s never sold at less than cost. If a product costs $100 to produce but the market only values it at $50, profit can be maximised simply by discontinuing it; if it costs $0 to produce then some value can be captured including it as part of a bundle. Equity research, like many information goods, fulfils both these conditions.

The problem is that the value of equity research and the value of trade execution ultimately flow to different parties. Although institutional investors notionally pay for both, the bundled fee comes out of the fund value, so the cost is borne by end-investors. End-investors typically pay fund managers a fee of 0.50%, say, for their services and cover the costs of trade execution out of their fund value. While there’s no doubt that they benefit directly from trade execution, it is moot whether they derive benefit from the equity research—that benefit stays with the investment manager. Consequently there’s an argument that investment managers should pay for it directly, out of their 0.50%. Indeed, because they’re not paying for it directly, investment managers may tend towards overconsumption of research.

Valuing equity research means solving a principal-agent problem buried inside a bundling problem.

To address this issue European regulators came along in 2018 and unveiled MiFID II—the second Markets in Financial Instruments Directive. The directive sought to unbundle equity research from trade execution. Investment managers and brokers are required to establish separate fee schedules for trade execution and research, with investment managers paying for research either out of their own P&L or else via an explicit charge to their end-investors.

The rules have been in place for two and a half years now. During that time, research budgets have been slashed, confirming that equity research was probably over-consumed in the first place. Some estimates suggest that investment managers’ research budgets have fallen by an average of 30% following the introduction of MiFID II. Many analysts have left the industry.

However, as in all regulatory interventions, unintended consequences emerged. Two in particular stand out.

First, although regulation required pricing to be unbundled, it didn’t require profit to be unbundled. In other words, firms remained free to cross-subsidise between product areas. The incentive to offer research at very low fees as a loss-leader for trade execution stayed—it was just more transparent. This gave larger firms with more financial flexibility a clear advantage. Regulation worked to make the big guys bigger.

Second, equity research performs a host of different jobs. They’re not all sustainable—Spitzer certainly made one of the more flaky ones redundant. But one that has survived is the public role that equity research plays in keeping companies in check. It benefits everyone with an interest in functioning markets that scores of analysts are engaged in the scrutiny of company financial statements; and crucially that they are not paid to do it by the companies themselves. Newspapers do it in politics; equity research does it in business.

Before MiFID II this role was funded privately as part of a bundle. Cleave the bundle apart and no-one may want to pay for it anymore. In particular, in the small cap segment of the market, where trading commissions are low, there is little incentive for equity research to provide coverage. Sure enough, a recent study found that 8% of European companies lost research coverage in the first year after the implementation of MiFID II.

The development highlights a hidden danger in unbundling regardless of the transparency it unleashes. Rory Sutherland cautions against the trend within tech to unbundle services into their core jobs: “Replacing a hotel doorman with an automatic door ignores the doorman’s wider remit—and value to hotel and customers alike.”

Regulation is always about trade-offs. Ben Evans makes the point well in his recent essay about technology: “You can have cheaper food or more sustainable food supply chains; you can make home-owning a wealth-building asset class or you can have cheaper housing. As voters, of course, we want both—I want my parents’ home to appreciate and the home I plan to buy to get cheaper.” MiFID II is one outcome of the trade-offs made in equity research.

Under cover of Covid, European regulators are now rolling back on unbundling. Proposed revisions to MiFID II are being introduced to facilitate research on small companies below €1 billion in market cap, making it easier for them to raise capital. Unbundling of fixed income research will be done away with altogether.

Similarly in the US, regulators don’t seem to like the idea of unbundling. When the chair of the Securities and Exchange Commission floated the idea in 2007 it failed to gain traction. More recently the SEC extended out to 2023 an exemption for US firms from being bound by MiFID II.

If there’s one silver lining from the process, it’s that research quality has improved. It’s difficult to measure quality but several studies concur. Fighting over limited available resources from investment managers, research analysts compete more directly in the quality domain. Even if MiFID II is unwound, the forced process of attaching a value to research should leave this dynamic intact. This is a good development for smaller and even solo research operators who were never able to compete on quantity. With technology solutions emerging to meet their distribution needs, they have capacity to create strong franchises.

Several platforms are already exploiting this. Seeking Alpha announced that its Investor Marketplace hit US$10 million in annualised revenue in January. The company takes a 25% cut leaving 75% for the independent analysts on its platform. Other research aggregators include Smartkarma and StockViews.

And then there’s the platform you’re reading this on. Last week a family office investor tweeted this:

In the old days I needed a sales force to fax, mail and precis my research out to clients. Today I can do it myself.

More Net Interest

Chinese Retail Investors

My most popular Net Interest so far was a note about retail stock trading in the US. It’s a trend that has taken hold in China, too, except there it’s more systemic. At the end of June China had 167 million retail investors, 12% of the population. They collectively own 29% of the Chinese market, a lot more than institutional investors, who own 17% (the rest is owned by corporates).

A study by the Shanghai Stock Exchange shows how badly retail investors perform. Between January 2016 and June 2019 they mostly booked losses in their personal trading accounts, while institutional investors were up 11%. The reason is overtrading. Although they own less than 30% of the market, they make up 80% of trading activity. According to the report, “With speculative and gambling motion, many of them tend to trade frequently. But the more they trade, the more they lose.”

As I pointed out in the original Net Interest note, there is a spectrum between stock investing and betting. For some firms it’s clear where they are positioned along the spectrum. DraftKings for example is plainly at the betting end. Others like the CFD brokers in the UK (IG Group and Plus500) offer financial products but sit closer to the betting end than the investing end. Robinhood is moving the centre of gravity in the US, it’s just less transparent about it.

Gold Financing

A favourite Net Interest theme is that financial companies are a window on everything—largely because they finance everything. In the past we’ve looked at the state of the economy through the lens of banks, and the airline industry through aircraft lessors.

Gold provides another window. Its rising price is benefiting one bank, Muthoot Finance. Headquartered in Kerala, India, this is the largest gold financing company in the world. It operates out of 4,500 branches across India, lending small sums to consumers.

The economics of the business are quite simple. Customers come through the branches looking to raise funds off the value of their gold jewelry. The bank lends them up to 70% of the value of their gold, at an average ticket size of around US$600. Loans are extended for a year although they typically redeem after about four or five months, and the bank earns a 12% spread. Around 80% of customers are repeats although recently the bank has seen an increase in first timers looking to raise some extra cash. Loan losses are historically quite low because of the sentimental nature of the collateral and also because its value is easy to realise in the event of default.

Rural India, where credit access is more limited, accounts for two thirds of the country’s total gold stock. The rising price of gold increases wealth in these areas so if it can be made liquid it comes at an opportune time.

Monzo

The UK challenger bank filed its annual report this week. Historically headlines had been about its growth. In March it was up to 3.9 million customers. But the report unveiled a new headline:

“Due to these obstacles, the Directors recognise there are material uncertainties that cast significant doubt upon the Group’s ability to continue as a going concern.”

The company faces three obstacles. First, top-line growth has slowed. As I highlighted in the very first Net Interest, Banks vs Fintech: A Coronastory, the acceleration in digitalisation caused by Covid should have been a boon to digital banks. Yet according to Monzo, “we’ve seen organic customer growth slow as word-of-mouth drops” (I guess people have got other things to talk about these days than Monzo).

Second, credit losses are emerging. The bank wasn’t much good at credit anyway. At the end of February, 20% of its loan book had either gone bad or was at ‘high’ or ‘very high’ risk of going bad. It’s so-called ‘stage 2’ and ‘stage 3’ loans, which are calibrated across all banks reporting under International Financial Reporting Standards, made up 25% of its loan book. This compares with 13% in Lloyds’ retail bank four months later.

Finally, the company specifically cited regulatory reviews around financial crime. Greater regulatory scrutiny represents an invisible asymptote for startup fintech companies. Once they get to a certain size it matters more, and it’s a big fixed cost, as Monzo is finding out.

(Image: Bundled by Robert Moran)

As a former sell sider for 10 years and now a buysider for 18 years, this is a great piece of writing. What the street offers is greatly commoditized. They all need to demonstrate their “onlyness” except they can’t figure out what that is. Zero imagination.

I really enjoyed reading your insights, especially your approach on providing historical context which is so important to deeply understand the business.

I have read your other posts on asset management and banking. I am wondering if you have a perspective on the future of wealth management, you touched on it one of your posts but wondering if you might do a deep dive similar to this one or the AWS of finance one. I ask for my own selfish reasons. I am in wealth tech and am trying to discern what the business might look like a decade from now given the cost pressure and regulatory environment.