The Art of Short Selling

Plus: Deutsche Bank, Custodia Bank, Late Fees

Welcome to another issue of Net Interest, my newsletter on financial sector themes. This week we look at short-selling. Paying subscribers also get access to comments on Deutsche Bank, Custodia Bank and credit card late fees. To join them and unlock that content as well as a fully searchable archive of 100+ issues, please sign up here:

“A market without bears would be like a nation without a free press. There would be no one to criticise and restrain the false optimism that always leads to disaster.” — Bernard Baruch

Among all the activities in finance, short-selling remains one of the most misunderstood. To many, the practice of selling something you don’t own with the intention of buying it back later at a cheaper price appears…abstract. Few baulk at the idea of buying low and selling high, but reverse the chronology and it sows confusion.

Even the Wall Street Journal, a business-focused newspaper of record, often has to explain the concept to its readers. When Russia’s central bank banned short-selling at the outset of the war on Ukraine, the Wall Street Journal reported that the regulator had “ordered brokers to stop allowing traders to place bets against Russian shares, a practice known as short-selling.”

It went on: “Short sellers borrow stocks they believe are overvalued and immediately sell them, hoping to repurchase the shares for a lower price when they need to be returned and to pocket the difference.”

Short selling is as old as markets. For as long as centralised markets have existed, traders have hedged risk and speculated on prices. But because they profit from bad news and exercise such apparent trickery putting on positions, short sellers in the stock market are cast as easy villains.

The first short seller was Isaac le Maire, one of the founders of the Dutch East India Company. After coming into conflict with his fellow directors, le Maire stepped down from the company and began to bet against it. As the stock fell, he and other short-sellers became scapegoats. In 1610, the company’s directors wrote to the government stating that “bear attacks, which generally assume the form of short selling, have caused and continue to cause immeasurable damage to innocent stockholders, among whom one will find many widows and orphans.”

It’s a theme that has rattled through the ages. At a hearing into the collapse of Lehman Brothers three weeks after it filed for bankruptcy, former CEO Dick Fuld blamed a number of “destabilising factors”, among them, short selling. In a recently-published memoir, his counterpart at Morgan Stanley accused short sellers of “destroying a storied franchise, built over almost three-quarters of a century of hard work and integrity.”

Similar opprobrium was levelled against another short-seller this week, Hindenburg Research. The firm took a short position in securities linked to Adani Group, one of India’s largest conglomerates, and published a report accusing the company of accounting fraud. Adani shot back with an attack of its own. In particular, it called into question Hindenburg’s motives. “Hindenburg has not published this report for any altruistic reasons but purely out of selfish motives,” it wrote, pointing out that, as a short seller, the firm would “book a massive gain” from a slide in Adani-related securities.

But from Hindenburg’s perspective, it took a lot of work to extract any gain. The firm’s report was the culmination of a two year investigation. And the risk of loss is high, with Adani “evaluating the relevant provisions under US and Indian laws for remedial and punitive action against Hindenburg Research.” If verifiably wrong, the firm’s reputation is likely to suffer more damage than getting an equivalent call wrong on the long side.

More generally, it’s not that easy making money from shorts. According to S3 Partners, a specialist New York-based consultancy that tracks short positions, short selling generated aggregate gains of $300 billion last year as stock markets fell. But that simply offsets some of the $572 billion of losses suffered over the previous three years.

And this year certainly hasn’t been kind.

“Short selling is for show, long investing for dough,” says former hedge fund manager, Russell Clark. But show doesn’t put food on the table, so why do short-sellers bother?...

The Art of Short Selling

Short-selling comes in various shades.

At the entry level, it can be used to hedge portfolios. Unlike mutual funds which maintain a pretty full exposure to the market at all times, hedge funds can adjust exposure by varying the amount of cash they carry or by putting on shorts to hedge some of their long positions. Some funds – so-called market neutral funds – go as far as to hedge out market exposure altogether. According to data compiled by Eurekahedge, these funds generated a 2.0% return last year, better than the market which was down 19.4% in the US. Since 2000, the strategy has outperformed the market – up 190% versus a market return of 160% – and, with only two down years and a maximum drawdown of 5.6%, it also strips away volatility normally associated with equity market investing.

Other funds maintain a long bias, albeit not as long as a mutual fund. According to Goldman Sachs, fundamental long/short funds on its platform ran an average of 48% net long in November last year – meaning that for every $100 of assets under management, their market exposure was just $48. This exposure reflects the combination of a leveraged long book, where positions make up 1.12x of assets under management, and a short book equivalent to 0.64x of assets. In other words, for every $100 of assets under management, these funds operate a leveraged long book of $112 and an offsetting short book of $64.

Unsurprisingly, given the downturn in markets last year, performance of long/short funds was not as good as market neutral – long/short equity funds in aggregate were down 8.4%. And what they eliminate in market risk, they make up for in basis risk. Imagine if the $64 of short positions went up at the same time as the $112 of long positions went down. Now you’ve got a $176 problem on your hands rather than a $48 one.

Increasingly, a lot of these funds use exchange-traded funds (ETFs) to engineer their short exposures, reflecting sector calls on the short side rather than stock calls. The funds on the Goldman Sachs platform managed an aggregate short book of $730 billion in November, but $180 billion of that was ETFs.

That’s not to say money can’t be made from single stock shorts. Last year, according to S3 Partners, short sellers booked profits of $15.8 billion on the sale of Tesla stock as the stock slid 65%. But consistently making money on the short side is hard. One reason is that stocks tend to go up over time: you’re not going to get multiple consecutive years of down 65% in a stock.

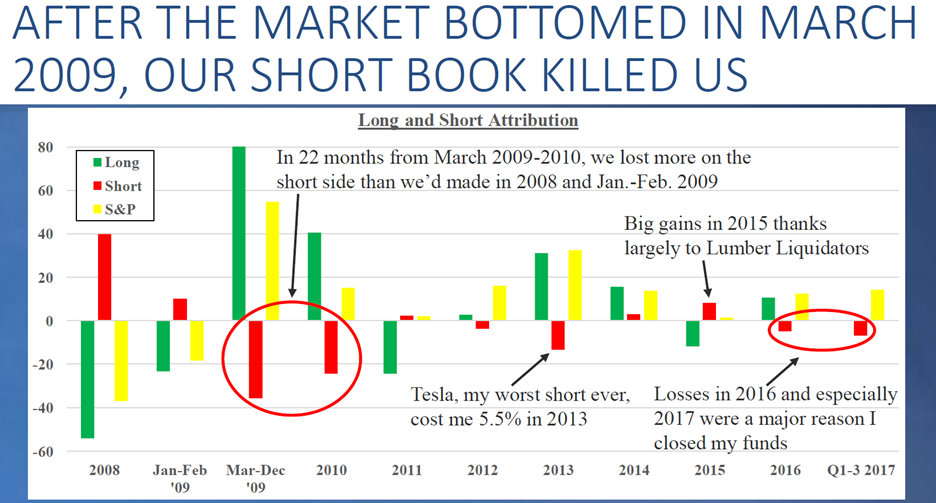

Take the case of hedge fund manager Whitney Tilson. Tilson started shorting in 2002. He slowly built his short book to 20% by the end of 2007. As the financial crisis took hold, he ramped up his short book to 60% by 2008. Over the next 12 months that paid off but then he lost it all. In the 22 months from March 2009 through to the end of 2010, he lost more money on the short side than he had made during the financial crisis. In the years that followed, he made small gains in three years, but lost more in the other four – including a 5.5% loss on Tesla in 2013, “my worst short ever.”

“Over my 15 years of short selling, I made a lot of money in 2008-early 2009 and 2015, but otherwise mostly took a beating,” he said. As well as losing a lot of money, his short selling activities also “sucked up a huge amount of time.”

Another reason short-selling is hard is the inverted risk/return profile it presents. Unlike long investing where upside is unlimited and downside is capped at your initial investment, in short selling the upside is capped at 100% and the downside is unlimited. This gives rise to very particular risk management challenges.

In his excellent book, Hedgehogging, former Morgan Stanley strategist and hedge fund manager Barton Biggs recounts the story of Jock Robinson, a (pseudonymous) fund manager whose speciality was “taking giant short positions in story stocks that had been promoted with what were wildly optimistic projections at best and frauds at worst.”

Robinson opened a short position in a company, Casino Resorts, whose stock promptly went up. As it went up further, Robinson added to his position, watching the price rise from 16 through 20 and 25 to 30. He put on an order to sell more if the stock ever got to 35. It did. Robinson was more convinced than ever that the company was overvalued but management presented well and the stock kept on going up.

As it touched 60, Robinson began getting calls to return stock he’d borrowed. In some cases, he couldn’t make delivery and he was bought in by hostile brokers, pushing the price even higher. Soon it hit 80. By then, Robinson had lost $100 million, knocking 22% off his fund in four months. He began to get frantic calls from clients with redemption requests, forcing him to buy back stock to cover his short or allow the position to become an even larger percentage of his fund. Sensing a death spiral, traders began speculating that there was a run on his fund and he would be forced to liquidate, requiring him to buy back more of his stock. The price went higher. Robinson’s prime broker demanded more margin as the position grew, forcing him to sell other stocks in his portfolio. Before long, Casino Resorts was 40% of his portfolio, its price now 90.

By this point, Robinson had had enough. He told his trader to begin buying back the stock to cover his short. News got out and the price rallied to 100. When he was done, Robinson’s fund had shrunk from $400 million to $80 million. He was all but out of business.

It didn’t matter that he was right. From the sidelines, Robinson looked on as the stock fell back to 60 after he’d stopped covering. Within two months it had drifted back to 45 and over the following years it fell to the mid-teens and settled in a range between 5 and 10.

Jock Robinson operated in the early 1980s, but his story is timeless. In 2008, short sellers were squeezed in Volkswagen; in 2021, they were squeezed in GameStop.

And Robinson didn’t even have to contend with disclosure requirements. While rumours got out about his positioning, nothing was officially broadcast. These days, many jurisdictions require funds to disclose their shorts. In the UK, a public share notification must be made when the net short positions of shares reach 0.5% of the issued share capital of the company concerned. The results are published daily in an Excel spreadsheet. Right now, for example, the biggest short in the market is Odey Asset Management’s short in Metro Bank.

Even where disclosures are not required, levels of short interest are broadly known and it often makes sense to avoid shorting stocks with high short interest. Even if you have capacity to bear some volatility, you may not want to be short the same stocks as Jock Robinson when he is liquidating.

Activist Short Selling

At his 2006 shareholder meeting, Warren Buffett reflected on the difficulty in managing shorts. “There’s nothing evil, per se, about selling things short,” he said. “I would say that it’s a very, very tough way to make a living. It’s not only often painful financially, it’s very painful emotionally.”

He goes on: “I’ve probably had a hundred ideas of things that should be shorted, and I would say that almost every one of them have turned out to be correct. And I’ll bet if I’d tried to do it and make money out of it, I probably would have lost money, I would have had no fun, and the opportunity cost…would have been enormous. Because if somebody’s running something that’s semi-fraudulent, they’re probably pretty good at it and they’re working full time at it and they’ve succeeded for a while and they may keep succeeding. And if they succeed and you go in at X and it goes to 5X, you know, all you’re hoping after a while is that it goes back to X again or something of the sort. It’s a very tough psychological game to play. Few people may be well-suited for it.”

Buffett has a point. When David Einhorn won a charity lunch with him in 2003, Einhorn wanted to discuss a short he’d recently put on in Allied Capital. Buffett observed that while Allied is just one position in Einhorn’s portfolio, for the company and its management, it is the whole ballgame, so they will say and do things an investor wouldn’t in order to win. Five years later, Einhorn wrote up the saga of his Allied short in a book, Fooling Some of the People All of the Time. Managing it had consumed an enormous amount of his time as the company fought back and encouraged regulators to investigate Einhorn for stock manipulation. “As a short, it hadn’t been what I expected, but it hasn’t been a disaster either,” he wrote in his first edition.

Financially, he did better than others. John Hempton, the hedge fund manager who tipped off FT journalist Dan McCrum to look at Wirecard, has admitted that he never made any money on his Wirecard short. Ennismore Fund Management, whose manager Leo Perry also helped McCrum in his investigative work, did manage to eke out a small profit of around $10 million on a fund size of $500 million. But that was after six years of work. “Is it worth it?” says Perry. “I have to say yes, because I’m still in the business. But I wouldn’t recommend short selling if you want a stress-free life.”

As well as long-short investors, Buffett highlights another kind of short seller, the specialist short-selling fund. “I would never put any money with a short fund, but not because I would think it would be ethically wrong. I just think they’re unlikely to make money.”

Specialist short funds emerged in the early 1980s. The first, Feshbach Brothers, was founded in 1982 by twins Joe and Matt Feshbach and colleague Tom Barton. At its peak, the fund managed $600 million. The Brothers perceived themselves as hype detectors serving an important watchdog function for the public. They looked for shorts with four characteristics: overvaluation, a fundamental problem at the company, weak financial condition, and weak or crooked management. “We short stocks where the negatives so overwhelm the positives that, over time, the market can’t just shrug off the bad news – eventually the stock price will reflect it,” Joe Feshbach told Kathryn Staley, the author of The Art of Short Selling.

Their first short was Universal Energy whose stock they thought was being manipulated by insiders. The stock crashed quickly and created a model for subsequent ideas. The Feshbachs undertook intensive work which sometimes led to information overkill. But they didn’t find company visits or talks with Wall Street analysts useful: “The company didn’t get to be a good short without management’s help.” These days, companies subject to short-selling often complain that funds don’t come to meet them before revealing their positions. But that’s precisely the point; in a market environment in which all information is necessarily in the public domain, the right to reply does not exist.

Jim Chanos was also early into the specialist short-selling market, setting up his fund Kynikos Associates in 1985. Chanos received acclaim for identifying fraud at Enron, riding the stock’s decline from an average $79.14 in 2000 through December 2001, when it collapsed to 60 cents. Ten years ago, he was managing over $5 billion but the rise in markets has taken its toll; at its most recent filing date (March 2022), assets under management at his fund were down to $288 million.

To mitigate their risk and effect a share price reaction, short sellers increasingly publicise their positions by publishing reports. Last year, according to Breakout Point, 113 new major short campaigns were launched, on average leading to 31% price declines following the release of the report. In 33 cases, the decline was higher than 50%. So far this year there have been several more, including Hindenburg’s report on Adani.

The model leads to heavy criticism by companies subject to it, but in helping to police markets, disseminating research widely fulfils an important role. “We’re not critical of this company because we are short; we are short because we are critical of this company,” said David Einhorn.

Even with an activist bias, it is still difficult for short-sellers to make money. “I could have made a lot more money with a lot less trauma if years ago said we’re going to do a long oriented fund,” says Carson Block, founder of short-selling firm Muddy Waters Research. But the people who do it have other incentives. “We probably have a belief…that we’re smarter than a lot of the people around us, even the people who are more successful and more popular than we are, and we probably ha[ve] a burning desire to show them up!”

Over the years, short-sellers have put the spotlight on Enron, Lehman Brothers and plenty more bad companies. In so doing, they improve price discovery for all market participants while helping to combat fraud. As interest rates rise, the return on cash that short-sellers receive when they sell stocks goes up, making short-selling structurally more profitable. That, and the success of firms like Hindenburg, will likely draw more capital in. Everybody is better off for it.

Thanks for reading! If you enjoyed this piece, please hit the “Like” button. Better yet, join the community by signing up as a paid subscriber!