Supply Chain Finance: Greensill and the Stillbirth of a New Asset Class

Plus: Europe vs the US, PEPSI vs Visa, Great Quarter, Guys!

Welcome to issue #7 of Net Interest, my newsletter on finance industry themes. Each week I deep-dive into one theme and highlight a few others.

This week’s deep-dive is a bit different — it’s co-written with my friend Steve Clapham. Steve is an expert in forensic accounting and runs an investment research and training consultancy, Behind the Balance Sheet. We take a look at Greensill, on paper one of the most valuable fintechs in Europe. What a story! It’s got it all: a Softbank angle, a BaFin angle (remember Wirecard last week?), a human interest angle (farmer turns billionaire) and for the wonks, a financial engineering angle.

This one’s a long one (12 mins reading time) which means it could cut off mid-email — you may want to click through to read on the Substack site.

Before we delve into the details, we need to provide some context, because what Greensill is trying to do is nothing short of launch a new asset class…

Supply Chain Finance: Greensill and the Stillbirth of a New Asset Class

New asset classes pop up all the time. Some, like common stocks, hit the big time; others fizzle out. What makes some asset classes durable and others a flash-in-the-pan is an interesting question.

Take eurobonds. These bonds, issued by companies in a different country and currency to their own, never existed before the early 60’s; they now make up a multi-trillion dollar market. They were devised by a team of bankers working for SG Warburg in London (now part of UBS). Their idea was to match the offshore dollars floating around in Europe, particularly Switzerland, with European companies seeking financing, all in a tax efficient way. The very first eurobond deal was completed in 1963 for Autostrade of Italy for US$15 million. Within four years the market had mushroomed to over a billion dollars and today it is one of the biggest markets in the world.

The insight the SG Warburg bankers had was simple. On the one hand there was a massive supply of dollars sitting outside the US, not doing very much (estimates suggest a figure of US$3 billion in 1962). On the other hand companies were looking for cheaper ways to raise finance than they could get in tightly regulated New York. Supply and demand. The eurobond was a mechanism to bring them together and its tax efficiency gave it impetus.

Twenty years later a similar thing happened in leveraged buyouts. Buyouts had been a thing for a while but it wasn’t until Jerome Kohlberg, Henry Kravis and George Roberts got together to form KKR did the market really take off. The dominance of KKR in the market in the 1980’s is really quite striking as this tweet attests.

The authors of the book The New Financial Capitalists explain KKR’s secret sauce:

“What separated KKR from the pack of buyout specialists was its peculiar ability to adapt the technique to new opportunities in fast-changing economic and financial environments. KKR also proved adept at cultivating trust with debt and equity investors, on the one hand, and target companies and their managers, on the other. In the process, KKR drove the scale and scope of the leveraged buyout to unprecedented heights, culminating in 1988-89 with the US$31 billion financing of RJR Nabisco…”

The origins of the two markets, eurobonds and leveraged buyouts, share a couple of features. The first, peripheral one, is that they were devised by outsiders. SG Warburg was a newish firm in the City of London, founded in 1946 by a German Jewish refugee; KKR was a start-up founded in 1976 after its founders left Bear Stearns. The second, central one, is that the markets were grown with equal attention to the supply side and demand side. Just as SG Warburg had done, KKR proved adept at cultivating trust with investors on the one hand and target companies on the other.

Fast forward another twenty years to the mid 00’s and the subprime mortgage market is running at full tilt. Initially that market had been nurtured responsibly. Borrowers who were less creditworthy nevertheless needed credit to finance home purchases and a market developed to allow them to do so. However, soon the dynamics of the market shifted and the demand for yield plus high credit ratings outstripped the supply of the borrowers who provided the raw ingredient. Underwriting standards slipped, NINJA loans (no income, no job, and no assets) crept in, and the rest is history. This time the growth in supply and demand were not kept in balance.

In the era of zero interest rates the pace of new asset class formation has increased. There’s crypto, of course (like eurobonds and leveraged buyouts, devised by an outsider). There’s marketplace lending, insurance-linked securities, litigation finance, aircraft lease securitisations; the list goes on. These new asset classes are typically characterised by a superior yield (except in the case of crypto) and low correlation with other asset classes.

One new asset class worthy of investigation is supply chain finance. Its pioneer is Greensill.

What is supply chain finance?

Supply chain finance is also known as reverse factoring. Here’s how it's described on Investopedia:

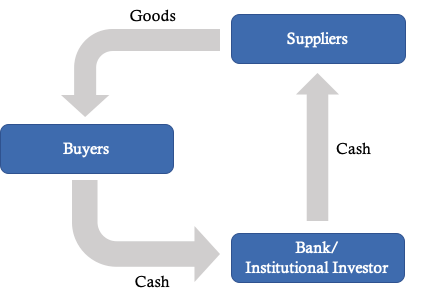

“Supply chain finance (SCF) is a term describing a set of technology-based solutions that aim to lower financing costs and improve business efficiency for buyers and sellers linked in a sales transaction… Under this paradigm, buyers agree to approve their suppliers' invoices for financing by a bank or other outside financier… By providing short-term credit that optimizes working capital and provides liquidity to both parties, SCF offers distinct advantages to all participants. While suppliers gain quicker access to money they are owed, buyers get more time to pay off their balances. On either side of the equation, the parties can use the cash on hand for other projects to keep their respective operations running smoothly.”

If you are more visually inclined, this picture captures the gist:

If it can be unlocked, supply chain finance, or reverse factoring, is potentially a huge market. In 2015 McKinsey estimated the volume of financeable highly secure payables globally to be US$2 trillion. For intermediaries they estimated that could be worth US$20 billion.

Greensill

The biggest independent intermediary globally is Greensill. The company was founded in 2011 by Lex Greensill, a one-time farmer turned banker who did stints at Citigroup and Morgan Stanley before launching his own firm. There’s an entertaining article with more on Lex Greensill here but the highlights include private jets, links with a former prime minister and a £4,000 expense claim for clothes.

According to its website, since being founded the company has extended more than US$150 billion of financing to over 8 million customers and suppliers in more than 175 countries.

Here’s how it works. (This is the wonky bit; skip ahead to the Softbank section if you prefer.)

Greensill acquires payment undertakings from client companies and assigns them to a special purpose vehicle (SPV) which issues notes that are sold on to investors. In other words, Greensill takes the company out of its promise to pay suppliers and parks that promise in a new entity. Investors in the notes issued by this new entity include funds managed by Credit Suisse and GAM. Some notes are also retained on the balance sheet of a bank the group owns in Germany.

Greensill then offers to pay the suppliers of its client company before the respective due dates and settles the invoices at a discount using funds raised via the SPV. At legal final maturity, the company repays the SPV and the note is redeemed at par. In other words, investors put money into a pot. That money is used to pay a company’s suppliers today at a discount to what they are owed. When the invoice is actually due the company reimburses the pot with the full invoice amount. The discount, less Greensill’s take, represents the investors’ return.

GAM, the Swiss based asset management firm, set up a fund to invest in Greensill-sourced assets in 2016. The fund ran into troubles in 2018, discussed below, but before that it had assets of US$3 billion. Credit Suisse set up three funds over 2017 and 2018. According to their prospectus, the goal of these funds is to “provide stable and uncorrelated returns”. Demand for the funds last year was so high that a freeze was put in place because supply of investments couldn’t keep pace. Assets grew from US$2 billion to US$9 billion over the course of the year. The freeze was removed in March, but by then demand had evaporated — the funds’ assets as at end June have fallen to US$7.9 billion.

As well as distributing assets to investors, Greensill has a bank in Germany which acts as a warehouse for assets it chooses to keep. The bank, based in Bremen, was acquired in 2014. As at end May 2019 the bank had assets of US$1.47 billion. It is regulated locally by BaFin, the German financial regulator.

Softbank the Unicorn-Maker

Things really got interesting for Greensill last year, when it attracted a major investment from Softbank. It had received its first outside capital from General Atlantic a year earlier but in 2019 it received an injection of US$1.4 billion from Softbank in two tranches. The deal valued the company at US$3.5 billion, leapfrogging it into the top tier of European unicorns. On paper only Klarna and Revolut have bigger valuations in the European fintech space.

Except Greensill isn’t a fintech.

Which makes it difficult to comprehend the valuation. In 2018 the company’s UK business generated profits before tax of US$42 million on revenues of US$234 million. The UK is the source of most of the group’s revenues; the Australian parent generated US$238 million of revenue in 2018. So at US$3.5 billion the business was being valued at ~15 times revenues. That would be rich even for a supercharged tech story.

But Softbank sometimes appears to have a different perspective of what constitutes a tech company — office provider WeWork, hotel chain Oyo and now run-of-the-mill financing business Greensill. Supply chain finance involves complex payment processing, but in contrast to WeWork and Oyo, Greensill uses third party IT platforms for origination, structuring and servicing from providers such as Taulia. Whereas Adam Neumann used Softbank’s equity to catapult its growth trajectory, Greensill took €400 million of the Softbank money and downstreamed it to its Bremen-based bank in order to bolster its capital ratios. But perhaps Softbank saw an opportunity to use Greensill to help finance its other investments — read on.

A little more about supply chain finance

To understand how that help could be forthcoming, we need to understand a little more about supply chain finance. The problem with supply chain finance is that it is prone to abuse. Companies are able to stretch their trade payables, and have a financial intermediary intervene to pay their suppliers. Yet this does not have to be disclosed in financial statements.

This has two important implications — it reduces companies’ reported debt and it improves their return on capital employed, one of the most important metrics to professional investors.

Supply chain finance could be one reason why companies like Electrolux have been able to improve their cash conversion cycle, as shown in the chart. Note that the improvement as evidenced by the black line declining to zero has been driven not by an improvement in operating efficiency – stocks and debtors are flat relative to sales in the last 15+ years – but by stretching the time taken to pay suppliers.

It’s not clear whether Electrolux has been using reverse factoring but we know that other companies such as Vodafone do. That large companies such as this use it at all is surprising because this type of financial instrument is inevitably dearer than debt. If you borrow from a bank, and you are a creditworthy company, you will pay a lower rate for the money than if an intermediary is inserted in the chain — the financial system will still have to supply the funds but there is now an increased friction with all the associated costs. Therefore the primary incentive to use supply chain finance is to make your balance sheet look stronger than it really is.

In 2018 the UK construction company Carillion collapsed after reverse factoring had allowed it to label almost half a billion pounds of debt as ‘other payables’. Other high profile corporate collapses where the technique has been used include NMC Health, Brighthouse and Agitrade.

It’s something the accounting bodies are looking into. Last October, the Big Four accountancy firms wrote to the US Financial Accounting Standards Board pointing out that whereas typical payment terms with suppliers historically might have been 60 to 90 days, some entities today seek to negotiate payment terms with suppliers of up to 180, 210, or even 364 days, using supply chain finance as the bridge. Indeed, many companies using reverse factoring fail to disclose this, and those that do often have a single line buried deep in the notes, often without quantification.

A web of conflict

Since Greensill’s growth began to accelerate the firm has been embroiled in a series of controversies:

💥 The Vodafone controversy. Bloomberg reported last year that as well as throwing its invoices into a Greensill-sponsored supply chain finance fund, Vodafone also participated as an investor. In this way it acted as both a lender and a borrower in the transactions. It has been reported that at the end of 2018 Vodafone had a €1 billion investment in the fund. Vodafone’s treasurer later went to work as Greensill’s CFO.

💥 The GAM scandal. Greensill was at the centre of a scandal in 2018 which all but brought down GAM, the Swiss asset management firm. According to Financial News, between September 2016 and May 2018 Tim Haywood, a star fund manager at GAM, invested more than £2 billion into Greensill-sourced assets. A large chunk of them were tied to just one business, GFG Alliance, an industrial conglomerate headed by Sanjeev Gupta, previously a Greensill shareholder. The article reports that Haywood also used several hundred million pounds of client money to finance Greensill itself and accepted gifts from Greensill without disclosing them to his employer.

💥 And now, the Softbank question. Last week Credit Suisse revealed that it is reviewing several of its funds after yet more conflict came to light, this time involving Softbank. According to the FT, Softbank is an investor in the Credit Suisse supply chain finance funds to the tune of US$500 million. At the same time, the funds are investors in securities backed by loans made to Softbank companies. Four of the top five exposures in one of the Credit Suisse funds are Softbank companies, including Oyo Hotels. Then, to top it off, Softbank is also an investor in Greensill which sponsors this whole thing. As with Vodafone, investors turned out to be funding themselves, only this time the same investors had a stake in managing the process.

These conflicts shine a light deep into the business model of Greensill. They reflect a firm trying to jumpstart a market whose core growth just isn’t there. This gets us back to the idea of what it takes for a new asset class to take root. The SG Warburg chaps didn’t have to rely on Autostrade to buy its bonds. And the KKR trio didn’t have to rely on RJR Nabisco management to buy their leveraged loans (and not because they thought they were ‘funny money’, ‘play dough’, or ‘wampum’ — to quote Barbarians at the Gate). Net out the assets that feature on the supply side and the demand side of the ledger, and the underlying growth in Greensill’s supply chain finance market shrivels up.

When it comes to asset class innovation, Lex Greensill ticks the first box. He is an outsider. But he doesn’t tick the second — the growth in supply and the growth in demand are not in balance.

And that’s not all. Dig deeper still and more red flags emerge.

More red flags

🚩 Greensill’s UK holding company, Greensill Capital Securities Limited, has no employees (they are recharged from another group company) and five directors resigned on a single day, 22 January 2018. Of the five current directors, three have been appointed since 14 December 2018 and an additional director, appointed on the same day, only lasted four weeks. One of the forensic analysis tests employed by Behind the Balance Sheet is board composition. Red flags are:

Directors resigning en masse — it suggests a potential fundamental problem.

Directors who join and resign in a matter of weeks — it suggests there could be something they didn’t like the look of.

🚩 The company’s auditors are Saffery Champness. They had a turnover of £71 million last year, versus former auditor Grant Thornton’s £491 million. It’s quite unusual for a complex financial firm to be audited by such a small auditor. The audit fee was US$98k, up from A$40k when the revenue was just A$26 million — revenues x13, audit fee x3.5; there must be some fabulous economies of scale in auditing this type of business.

🚩 Bank analysts and regulators look out for a number of things. They don’t like excessive growth, and they don’t like expensive funding. Greensill’s German bank grew its loan book over 3.7x in the 17 months between December 2017 and May 2019 (latest available data). The bank funds its loans through time deposits which it secures through money brokers and retail platforms. Right now it offers 0.70% for a one-year deposit, the second-highest rate available from a German bank.

🚩 The Supply Chain Finance funds are managed by Credit Suisse rather than by Greensill which is presumably involved in the origination and execution of the trades. Its regulated subsidiary, Greensill Capital Securities is regulated by the FCA, and has had three directors authorised since August, 2017. The founder became an FCA-authorised individual on 25 November last year, and the regulated subsidiary has added a further dozen authorised individuals in the last 12 months. This suggests that Greensill is expanding into regulated activities, although somewhat surprisingly given the size of the group, the subsidiary is an appointed representative and does not appear to have an in-house Compliance function.

Conclusion

Pioneering new asset classes is hard. The authors of The New Financial Capitalists write, “The essential populism of American culture is uncomfortable with financial schemes, which have so often been associated with venal fraud and scandal, or worse, unfruitful labour.”

In the case of supply chain finance it is not clear there is natural demand and so pioneers need to shimmy it along. The result is an institution drawn to scandal which itself raises several red flags. No-one comes out of this looking good — not the pioneer, nor its main investor, nor the companies it services (indeed, with several of them having gone bust, stock pickers could do worse than to screen the rest for ideas). Perhaps it takes more than a zero interest rate environment to spawn a new asset class; perhaps authentic new asset classes only come along once every twenty years.

More Net Interest

Europe vs the US

Europe has lagged the US for so long now it’s almost become entrenched. Not since 2006/2007 has economic growth in Europe been as strong as in the US. But that may be about to change, and coronavirus is the catalyst.

Europe was initially hit harder than the US both from a health perspective and then, because of the response, from an economic perspective. Real GDP declined almost three times as much in the Eurozone in the first quarter than in the US.

Now, Europe is rebounding more quickly. Part of it is virus control. Dr Anthony Fauci understated it on BBC Radio this week: “If you look at the different curves between the EU, the UK and others, how they’ve handled the outbreak, they’ve had big spikes and then they brought it down almost or even to baseline in some countries. The situation in the US has been more problematic…”

A second reason is employment control. European short-time work schemes have cushioned the impact the crisis has had on unemployment. Finally, Europe has also taken the opportunity to address some structural factors — the north/south sovereign funding gap looks set to be closed by a European Central Bank pandemic programme and a Europe Commission Recovery Plan.

Goldman Sachs for one now estimates stronger growth in the Eurozone than in the US over the next two years. The only question is whether it’s a blip or reversion of a multi-year trend.

PEPSI vs Visa

When Visa demutualised in 2008 Europe didn’t want to take part. It remained owned by its 3,700 member financial institutions. Although it entered into a contractual arrangement with Visa Inc, it operated different systems and retained independent control. However a financial structure was put in place that gave Visa Europe the option to sell to Visa Inc at a predetermined valuation. In 2015 that option was exercised and six months later Visa Europe’s owners cashed out and Visa Inc became global.

Now European financial institutions want to start all over again. They have got together to form a Pan European Payment System Initiative (or PEPSI) to handle all forms of cashless transactions without using either Visa or Mastercard networks. There’s a framework in business that money can be made either by bundling or unbundling. At the level of corporate strategy an alternative formulation could be that money is made by building up or by spinning off. It does seem like a waste of energy though.

Great Quarter, Guys!

Well that’s another quarter wrapped up and for investment banks, it’s been a good one. Jefferies has already reported its quarter to end May and churned out record sales and trading revenues. Overall trading revenues almost doubled versus last year, and within that fixed income trading revenues almost tripled. Investment banking fee income has been strong, too. The FT reports that fee income hit a record in the first six months of the year as companies tapped the debt markets to tide them over the coronavirus crisis. All of which bodes well for Goldman Sachs, Morgan Stanley and the others.

What’s surprising is that this normally wouldn’t be happening at this stage of the economic cycle. Looking at the economic data, we’d typically expect trading and investment banking revenues to be down 20-30%. That expectation was built into the Fed’s stress test, which paired 10% unemployment with a market down 50%. (In real-life, unemployment is 13% and the market is down 8%). Clearly the Fed is the missing link here. Its actions have supported banks’ trading profits. And in that they have validated the universal banking model — the boom in trading offsets the bust in credit.

Brilliant Read as always Marc

I am going to be a regular on your substack now marc. This was a brilliant read.

One question, how do you keep track of all the financial related news across the world? Is there a go-to place for you to read or a list of websites you keep track of?