Money for Nothing

The Golden Age of Arbitrage?

It’s easy to miss The Arbitrager pub in London. Nestled between sandwich shops on the perimeter of Drapers’ Hall, a nineteenth century guildhouse not far from the Bank of England, it’s a small place with a narrow entrance and few seats. But pass by on a summer’s evening and you’ll see brokers, traders and… arbitragers (arbitrageurs?) gather along the ancient alleyway outside to discuss the day’s events, pints perched atop beer barrels. Not as many of them operate in the vicinity as in the pub’s heyday in the 1990s, but The Arbitrager continues to cater to the clientele it’s named for.

When it changed hands last year, the pub’s former proprietor bemoaned what a difficult business it is to run: “Pub and bar ownership isn’t for the faint hearted,” he said – it “requires energy and focus.” It’s something his patrons might say about their own business. The difference is that while the hospitality industry faces challenges (as I know well – I’ve described my own experiences of owning a pub here before) the arbitrage industry is on a roll: a “golden age,” the Financial Times characterized it this week.

The concept is simple enough. “Arbitrage is when you can do a set of different trades that cancel each other out and make a free profit at the end,” one likely former customer writes in his book, The Trading Game. He was looking at foreign exchange, but the breadth of such trades is currently huge:1

Disrupted by the crisis in Iran, the spread between oil prices in different parts of the world has rarely been wider. Last month, a barrel of crude oil could be picked up for $78 in Kansas; in Sri Lanka, it cost $286.

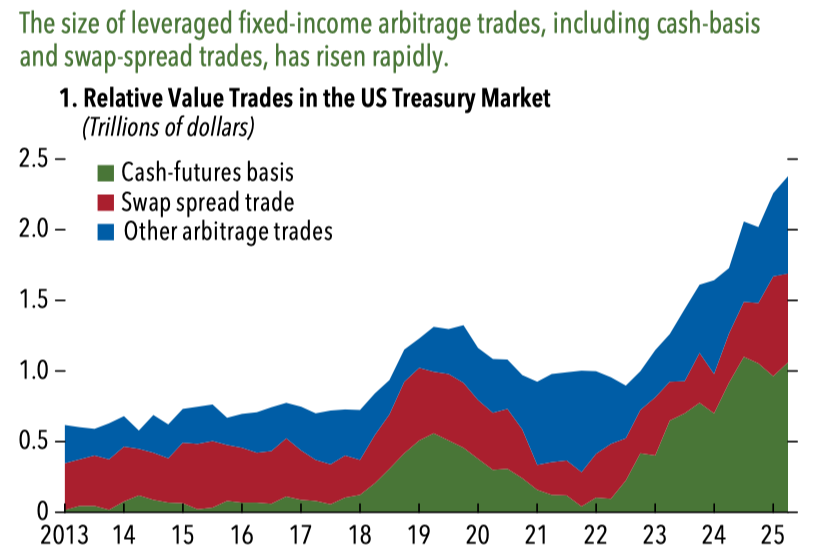

The so-called “basis trade” where traders sell Treasury futures and buy underlying Treasury bonds continues to attract record flows, estimated at over $1 trillion. It profits when the basis between the two instruments converges, often at the futures’ expiry. The International Monetary Fund (IMF) calculates that after a period of low profitability from 2020-23, returns rose to nearly 2% on numerous occasions in late 2024 and 2025. With leverage, that becomes meaningful.

Fixed income markets provide a venue for other arbitrage trades, too, including the swap spread trade which exploits the difference between the fixed rate of an interest rate swap and the yield of a government bond. Including the basis trade, The IMF estimates that traders have around $2.3 trillion of fixed income arbitrage exposure on their books right now. So far it’s been a good risk-adjusted trade – since September 2022, the Bloomberg Fixed Income Arbitrage Hedge Fund Index is up 32%.

The growth of private markets creates new opportunities. We’ve discussed the wave of redemptions that has hit private credit funds over the past few months. Some of that is being recycled into publicly traded funds that trade at steep discounts to net asset value.

For those putting on or facilitating these trades, it’s a profitable time. Jane Street, whose legacy business lies in exploiting price differences between the market value of exchange-traded funds and their underlying holdings, earned a record $39.6 billion of trading revenue last year – more than any of the traditional Wall Street brokers. Glencore announced this week that first quarter profits put its trading unit on track to exceed the top end of its long-term guidance for the full year. And as a measure of how hedge funds are sizing the opportunity, their borrowing sits at a record high of $7.42 trillion, up a third over the prior year.

Arbitrage is a broad term and it’s often misused. If you want to sound clever in finance circles, simply describe your latest trade as an “arb”. To dig into what arbitrage really is, and how the opportunity is playing out, read on.